Accounting conventions are the rules and guidelines that govern the preparation and presentation of financial statements. These conventions ensure that financial statements are comparable, reliable, and useful to stakeholders such as investors, creditors, and regulators. There are several accounting conventions that are widely accepted in the financial industry, including the going concern principle, accrual basis of accounting, and materiality principle.

The going concern principle is the assumption that a business will continue to operate for the foreseeable future. This principle is important because it allows a business to record its assets and liabilities at their current market value, rather than their liquidation value. This convention is important because it helps to provide a more accurate and realistic picture of a business's financial position.

The accrual basis of accounting is the practice of recording transactions when they occur, rather than when payment is received or made. This convention is important because it ensures that all revenue and expenses are recorded in the period in which they are earned or incurred, rather than when payment is received or made. This helps to provide a more accurate and complete picture of a business's financial performance.

The materiality principle is the concept that financial statements should only include information that is material, or significant enough to affect the decisions of stakeholders. This principle is important because it ensures that financial statements are not cluttered with insignificant or immaterial information, which could mislead or confuse stakeholders.

In addition to these conventions, there are also generally accepted accounting principles (GAAP) and international financial reporting standards (IFRS) that provide further guidance on the preparation and presentation of financial statements. These principles and standards are important because they provide a consistent and transparent framework for the preparation and presentation of financial statements, which helps to ensure that financial statements are comparable and reliable.

In conclusion, accounting conventions are essential for the preparation and presentation of financial statements. These conventions ensure that financial statements are comparable, reliable, and useful to stakeholders, and they help to provide a consistent and transparent framework for financial reporting.

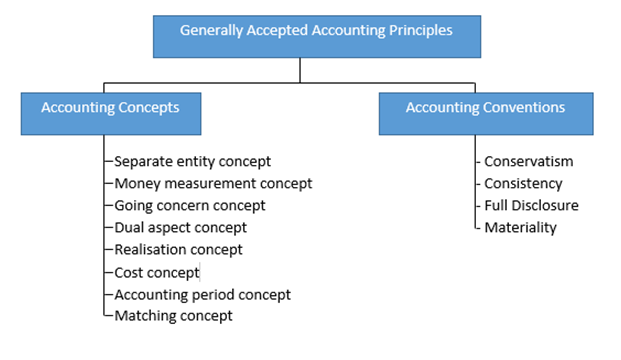

Accounting Concepts and Conventions

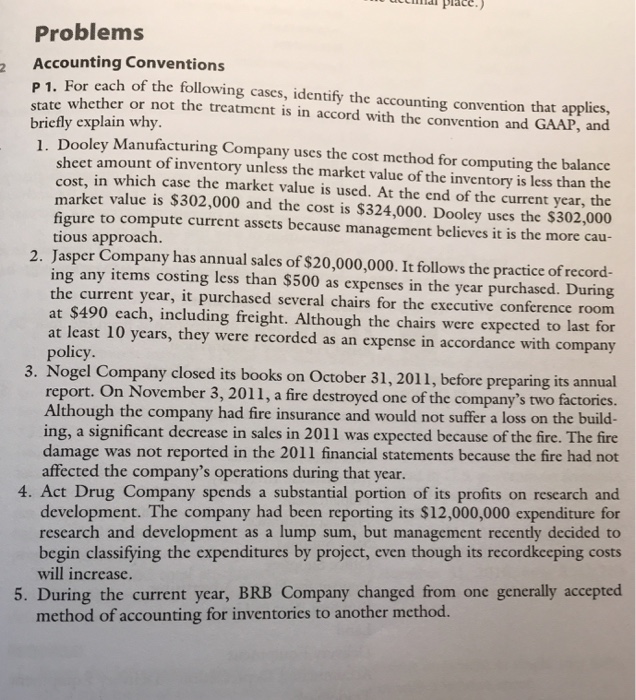

The net income of the company is Rs. And a proper disclosure of change in method of depreciation must be made, and accountants should also disclose its effect on statements. What do you mean by "anticipate no profit but provide for all possible losses"? But they help maintain consistent financial statements and an accurate balance sheet. At the end of the day, this helps maintain consistent financial statements. The business shall record all the expenses and liabilities when it sees uncertainty of incurring loss or liability.

What are the 4 accounting conventions? Convention of Disclosure The convention of disclosure implies that statements should be qualified enough to disclose all the relevant, material and potentially important information properly so that the reasonable users can make calculated decisions with the assistance of such provided information. Similarly, expenses are recognized at the time services are provided, irrespective of the fact that cash paid for these services are made. That means that when two values of a transaction are available, the lower one should be favored. If the method of accounting is changed from one period to another, it will make the comparison of financial statements of different periods difficult. Advertisements Financial statements are analyzed by various stakeholders as management, employees, debtors, creditors, governments, banks, etc.

What is Accounting Convention? Definition, Types, Pros and Cons

Full Disclosure The full disclosure accounting convention relates to relevant and important information. Every business recognizes the importance of accounting and the role it plays. Financial accounting is related to ascertaining the financial position of company. This convention sounds rigid, but it does not restrict an entity from changing any accounting principle or method. Disclosure In accounting, the convention of disclosure states that all material and relevant facts concerning the financial performance of a business entity must be fully and completely disclosed in financial statements and their accompanying footnotes. There are two types of accounting systems namely single entry system and a double-entry system. For example, in addition to Thus, the In financial accounting practice, information should not be judged on its size, but whether it is significant.

Accounting Conventions Definition Accounting conventions are the accounting practices and procedures that are commonly used in the preparation of financial statements. This allows for the reliable comparison of the financial results, financial position, and cash flows of many organizations. If any expense is below 5% of the net income, it can be considered immaterial. It implies that the fixed assets like plant and machinery, building, furniture, etc are recorded at their purchase price. For an investor, it is essential to go through all the information before making any decision. Going Concepts The Going concept in accounting states that a business activities will be carried by any firm for an unlimited duration This simply means that every business has continuity of life. Con sistency does not mean that there could not be made any change in accounting procedures, rather, consistency emphasizesthat if due to any reasons the change in accounting procedures is to be made then it should be disclosed in the financial statements.

The value of long term assets are amortized over their useful life. And How Does it Work? The expenses in the range of 5% to 10% are subject to the accountant's matter of judgement. What is the convention of conservatism? GAAP is used to describe rules developed for the preparation of financial statements and are called concepts, principles, conventions, and postulates, etc. These are the assets of the business and not of the business owner. Example: When inventory is recorded, accountants record it lower cost and the realisable value.

For example, if your business has lawsuits or contingent liabilities, the details must get included in adjoined notes. A bad debt provision refers to the reserve made by a company to set aside an amount computed as a specific percentage of overall doubtful or bad debts that has to be written off in the next year. Materiality In this convention, you only include relevant or important facts. This convention is important because it makes the financial statements of different accounting periods comparable. As the range and detail of accounting standards continue to increase, there are fewer areas in which accounting conventions can still be used. Hence, management needs to be concerned about the performance of the business and plan the accounting policies accordingly.

Difference Between Accounting Concept and Convention (with Comparison Chart)

The disclosure must be made in books of accounts about these legal proceedings as it will affect interest of shareholders and investors. Another relevant example for the Convention of Disclosure can be in the context of loans. Daniel Liberto is a journalist with over 10 years of experience working with publications such as the Financial Times, The Independent, and Investors Chronicle. Material information refers to facts, if those are being left out or interpreted in any other way other than what it is in the financial statements, it could lead to influencing the decisions of users of financial statements. Eventually, this helps them make more appropriate decisions and set more achievable goals. In the accounting system, the accrual concept tells that the business revenue is realized at the time goods and services are sold irrespective of the fact when cash is received for the same.

What are Accounting Conventions? What Are the 4 Accounting Conventions?

What is the going concern concept? However, specific GAAP rules are sometimes subject to different interpretations, and unscrupulous companies can find a way to bend or manipulate them to their advantage. For example, an investor wants to compare the financial performance of a business entity of the current year with that in the previous year. The commission should also be recorded in the same month. These principles assist businesses in establishing procedures to record business transactions that have not yet been fully addressed by accounting standards. The accounting convention that transactions are only recognized in financial statements if they can be measured in monetary terms. They may have options, but they do not implement them because of time, cost, habits, and practical benefits. The assets are not recorded at their market price.

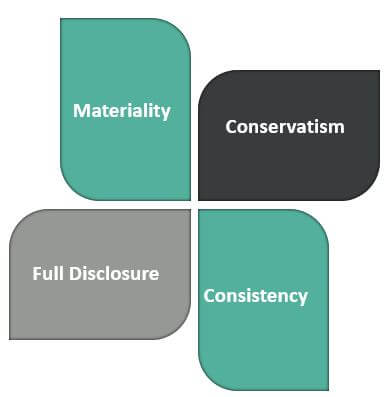

At the same time, it makes certain financial statements have all relevant information for the benefit of investors. The year that begins on January 1 and ends on January 31 is termed as calendar year whereas the year that begins on April 1 and ends on March 31 is termed as financial year. Going concerned , the Entity concept is some of the examples of accounting concepts. Thus making it easy for investors, creditors, and analysts to compare the performance of peer groups of companies. So this loss of 0. The most common accounting conventions are materiality, full disclosure, conservatism, and consistency. So, it considers both the makers and consumers of the financial data and assists them in every possible way.

The most common users to the financial statements are Management of the Company, Investors, Customers, Competitors, Government and Government Agencies, Employees, Investment Analysts, Lenders, Rating Agency and Suppliers. Another example that a business needs to disclose is why it has changed any accounting method or principle. What is an example of monetary unit assumption? Consistency According to the consistency concept, the practices and methods of accounting remain constant in different accounting periods. These are the fundamentals of accounting practice. Advertisements The proper explanations shall be provided under disclosures to the financial statements for changes in accounting principles and methods. Corporate Social Responsibility is managing the operations of the company in such a way that it produces positive impact on Society.