Actual overhead. The under absorption and over absorption of overhead — AccountingTools 2023-01-05

Actual overhead Rating:

8,7/10

1492

reviews

Actual overhead refers to the actual cost of indirect expenses that a company incurs in the course of conducting business. Indirect expenses are those that cannot be directly tied to the production of a specific product or service, but are still necessary for the company to operate. Examples of actual overhead costs include utilities, rent, insurance, and administrative salaries.

One of the key challenges for businesses is accurately forecasting and managing their actual overhead costs. These costs can vary significantly from month to month and year to year, making it difficult for businesses to accurately budget for them. Inaccurate budgeting can lead to financial difficulties for the company, as it may not have enough funds to cover its overhead costs.

To effectively manage actual overhead costs, businesses must have a thorough understanding of all the indirect expenses that they incur. This includes identifying all the various types of overhead costs, as well as the sources of those costs. For example, a company may incur overhead costs from maintaining its office space, such as utilities, rent, and property insurance. It may also incur overhead costs from its administrative staff, such as salaries, benefits, and training.

In addition to identifying and understanding the sources of actual overhead costs, businesses must also have systems in place to track and monitor these costs. This includes implementing effective financial management systems, such as budgeting and forecasting, and regularly reviewing and analyzing the company's financial performance. By doing so, businesses can identify areas where they may be overspending on overhead costs and take steps to reduce those costs.

Managing actual overhead costs is a critical aspect of running a successful business. By accurately forecasting and monitoring these costs, businesses can ensure that they have the necessary funds to cover their indirect expenses and remain financially stable. This, in turn, helps to ensure the long-term viability and success of the company.

Accounting For Actual And Applied Overhead

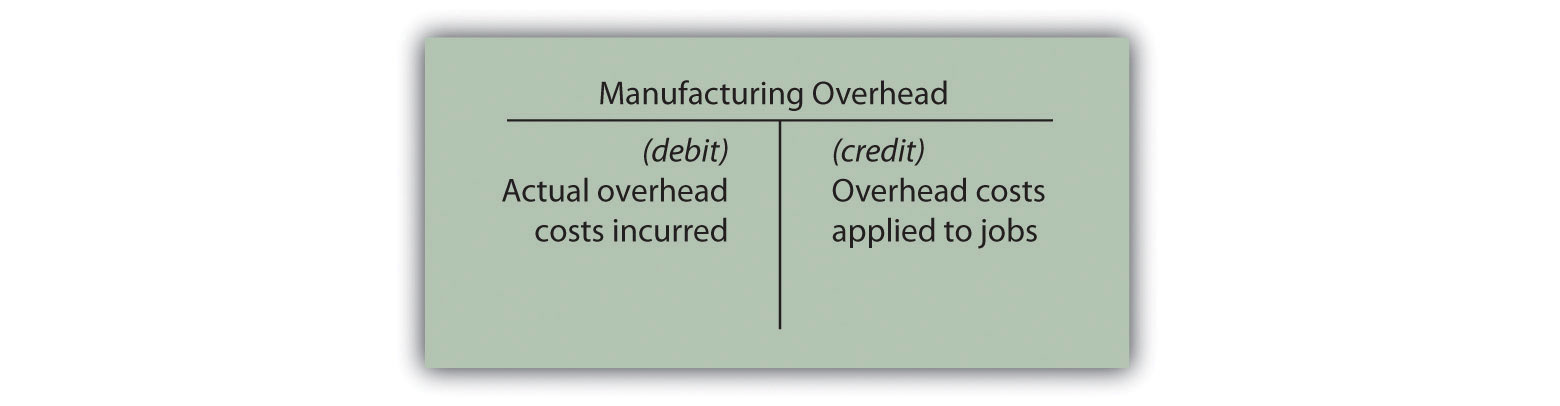

Overhead is calculated using a formula to ensure the appropriate allocation of the cost across products. Estimated overhead is not used here. Using the cost driver, companies can identify the exact cost during production and then properly allocate the identified cost to those units involved. To calculate manufacturing overhead, you need to add all the indirect factory-related expenses incurred in manufacturing a product. Calculate the amount of overhead that was overapplied or underapplied. Usually, these include accrued expenses, cash, and bank accounts. Keep in mind and applied overhead is an estimate.

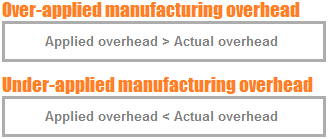

Compare applied overhead to actual overhead. Companies account for both types of overheads during different stages in the accounting process. If actual overhead costs from individual month is used, the overhead cost per unit will vary because of seasonal costs. Remember that applied overhead is what is in cost of goods sold right now. Budget or spending variance is the difference between the budget and the actual cost for the actual hours of operation. If overhead is underapplied, meaning you have too little overheard in cost of goods sold, add the amount that is underapplied.

The difference between actual overhead and applied overhead — AccountingTools

If you have the terminology clear, this problem is easy. But what happens when the actual bills start coming in on all those indirect costs? Some parent entities choose to accept all corporate overhead as expenses immediately and not allocate any costs. A predetermined overhead rate provides the only feasible method of computing product overhead cost promptly enough to serve management needs and eliminates uncontrollable and illogical month to month fluctuations in unit costs. Actual overhead is what should be in cost of goods sold. Accountants measure the differences between actual and applied overhead at the end of each period to ensure that applied overhead estimations are increasingly accurate each time.

Therefore, it tends to be wise for various units to work on their product or service proficiency to lessen overhead costs. Similarly, some companies will use a more accurate method of reconciling applied and actual overhead. Budget or spending variance measures the following: - the differences between the standard prices and the actual prices of manufacturing overhead materials and services - the difference between the standard and actual quantities used What are the formulas to calculate the overhead variances? Consequently, companies must determine the journal entries for that stage. For example, overhead costs such as the rent for a factory allows workers to manufacture products which can then be sold for a profit. Total overhead cost variance can be subdivided into budget or spending variance and efficiency variance.

Overhead: What It Means in Business, Major Types, and Examples

This way, they can create an associated double-entry. Applied overhead is what is currently in the account. The overhead is attributed to a product or service on the basis of direct labor hours, machine hours, direct labor cost etc. At the end of the accounting period, these actual overhead costs are reconciled with the applied overhead to make sure that the actual overhead costs end up in the cost of goods sold. Some materials used in making a product have a minimal cost, such as screws, nails, and glue, or do not become part of the final product, such as lubricants for machines and tape used when painting. Capacity Variance: Change in the utilization of capacity due to low demand, lack of power, and raw materials shortages, among other factors.

Other indirect costs include insurance and service costs. What is the difference between Actual and Applied Overheads? Since overhead is often considered a general expense, it is accumulated as a lump sum. Applied overhead is the amount that is added to the cost of goods sold, and is typically less than the actual amount. Direct labor and manufacturing overhead costs think huge production facilities! Related: What Is Underapplied Overhead? Corporate overhead accumulates into period costs, or expenses accounted for over a certain period of time in the business, and charges as an expense each period. Apply the formula Accountants usually can't trace every cost to its source, so they use the applied overhead formula to apply to cost objects and create an estimate for each period. Financial overhead, including property taxes, utilities, insurance policies, and management fees, is the most significant type of overhead expense.

Actual overhead varies depending on the company, but there are several key factors that contribute to it. These overheads get absorbed by each production unit. Identify the cost object Businesses incur costs that don't directly relate to the manufacture of a product or the creation of a service. The term refers to the costs that are added to jobs as they are completed. At the same time, accountants are also recording the actual bills. In accounting, all costs can be described as either fixed costs or variable costs.

What Is Applied Overhead? (Definition, Formula and Example)

Applied overhead is those costs for which it is impossible to directly apportion to a cost object, including insurance, compensation for administrative employees, rent. Wondering what a cost object is? One group is applying overhead based on the actual activity and the predetermined overhead rate. If too much overhead has been applied to the jobs, we say that overhead is overapplied. However, the same does not apply to overheads. Karl has also collaborated with respected publications in the manufacturing field, including IndustryWeek and FoodLogistics. A cost object is a particular unit of product for which cost is summed. This is why knowing the terminology is really important.

What is the difference between actual overhead and applied overhead?

Using a manufacturing overhead cost formula and calculating the total costs per unit will help you determine whether you need to adjust your selling price. Definition of Actual Overhead In the context of actual and applied overhead, actual overhead refers to a manufacturer's Actual overhead are the other than direct materials and overhead costs must be allocated, assigned, or applied to goods produced. Since the applied overhead is in the cost of goods sold at the end of the period, it has to be adjusted to reflect the actual overhead. At the end of the year or period, the applied overhead will likely not agree with the actual manufacturing overhead costs. These overhead costs being constant give a different per unit cost when divided by differing production volumes. Companies usually use the strategic methodology in their overhead application.