Difference between fixed and flexible budget. Difference Between Fixed and Flexible Budget (Top 9) 2022-12-19

Difference between fixed and flexible budget Rating:

4,3/10

1431

reviews

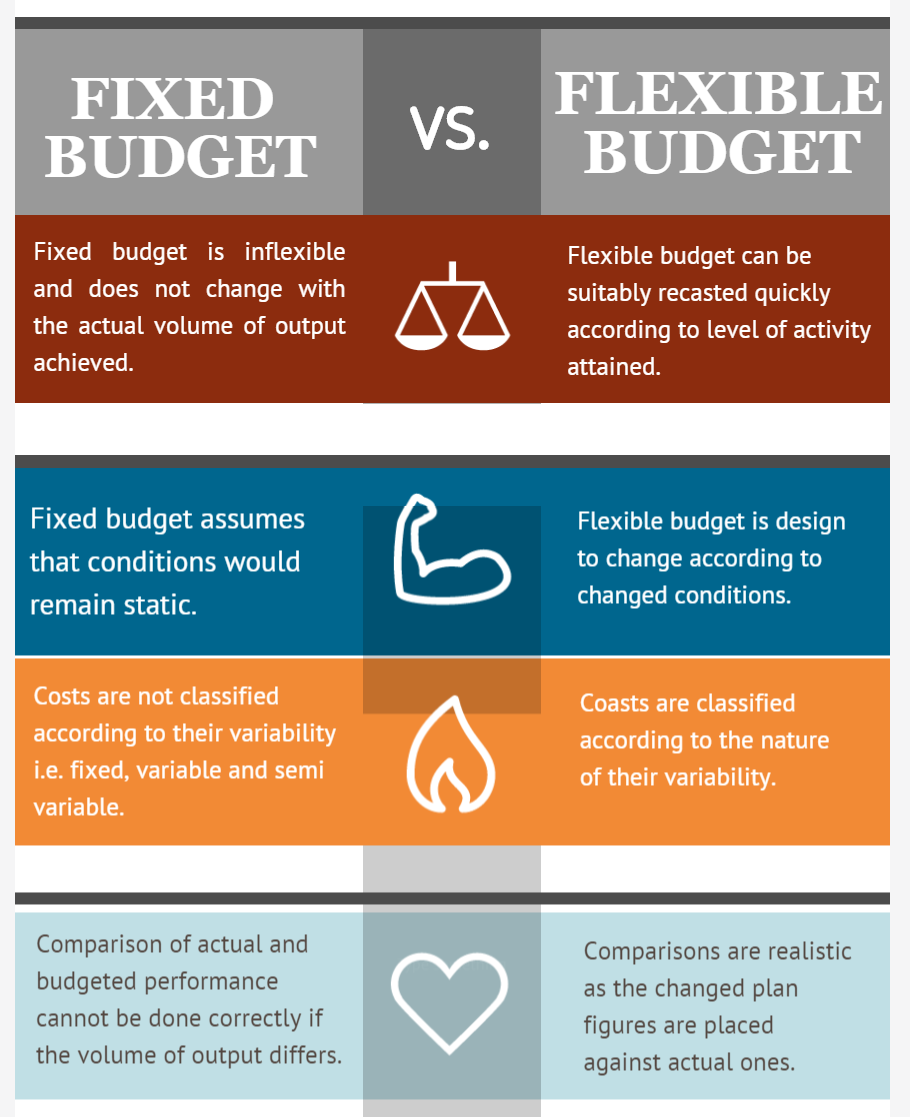

A fixed budget is a financial plan that outlines a set amount of money that will be spent on specific activities or expenses within a certain period of time. This type of budget is typically developed for long-term planning purposes and is not meant to be adjusted based on changes in actual performance.

On the other hand, a flexible budget is a financial plan that adjusts to changes in the level of activity or production. It is designed to be more responsive to changes in the business environment and is typically used for short-term planning purposes.

There are several key differences between fixed and flexible budgets:

Adjustability: As mentioned above, the main difference between fixed and flexible budgets is their adjustability. A fixed budget is set in stone and cannot be changed, while a flexible budget can be adjusted based on actual performance.

Planning horizon: Fixed budgets are generally used for long-term planning, while flexible budgets are used for short-term planning. This is because fixed budgets are not meant to be adjusted based on changes in actual performance, while flexible budgets are designed to be more responsive to changes in the business environment.

Variance analysis: Variance analysis is the process of comparing actual performance to budgeted performance. With a fixed budget, any variance between actual and budgeted performance is considered unfavorable. With a flexible budget, the variance is evaluated based on the changes in the level of activity or production.

Use in decision-making: Fixed budgets are often used as a benchmark for performance evaluation, while flexible budgets are more useful for decision-making purposes. This is because a flexible budget can be adjusted based on changes in the business environment, allowing managers to make more informed decisions about how to allocate resources.

In conclusion, fixed and flexible budgets are two different types of financial planning tools that are used for different purposes. Fixed budgets are used for long-term planning and performance evaluation, while flexible budgets are used for short-term planning and decision-making. Understanding the differences between these two types of budgets can help managers make more informed financial decisions and effectively allocate resources.

Fixed Budget vs Flexible Budget

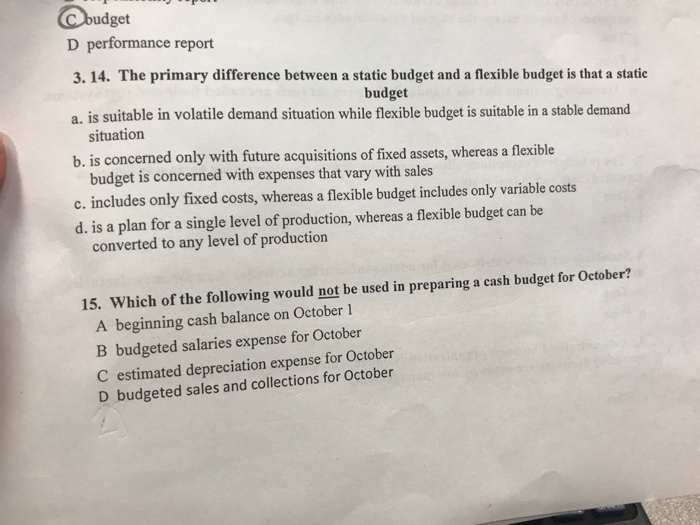

Unlike in a static budget, which is prepared for a single activity level, a flexible budget is more sophisticated and useful. Flexible budgeting, on the other hand, is particularly adaptable to company scenarios. For example, agricultural activities, wool-based industries, etc. Differences between fixed budget and flexible budget Differences based on Definition: A fixed budget, also known as a static budget, is a financial plan based on the assumption that particular amounts of commodities will be sold during a specific period. It is relatively complex to make since computations have to be made for all possible scenarios. In a flexible budget, we have to further divide mixed costs into their fixed and variable portions.

This is prudence, regardless of the scale of the Post navigation. Individual budgets will be prepared by each department, and the net outcome will be reflected in the master budget. It also serves as a measure of cost management. Some budgets are prepared for alternative output levels to show the amount of expense to be reached at each level of activity. With the help of a static budget, firms can assign money to resources that they expect to remain the same over the period specified. On the other hand, a flexible budget is estimated based on realistic situations.

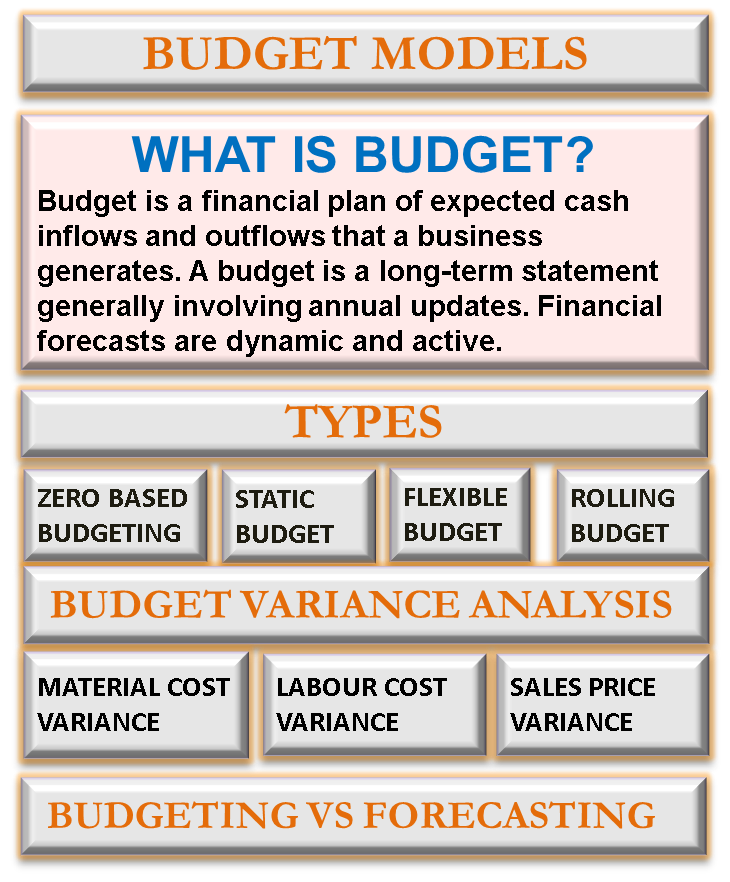

What Are the Differences Between Fixed, Flexible, & Zero Based Budgeting Processes?

However, regardless of the nature of a business, a fixed budget may still be useful as a way to control costs. Finally, mixed costs are those that have fixed and variable components to them. . A flexible budget is a budget that changes as per the necessity of activity level. The net variance in this example is mainly due to lower revenues. Also, other cash disbursements such as equipment purchases and dividends are listed. Figure 1: Components of master budget Operational Budget Operational budgets prepare forecasts for routine aspects such as incomes and expenses.

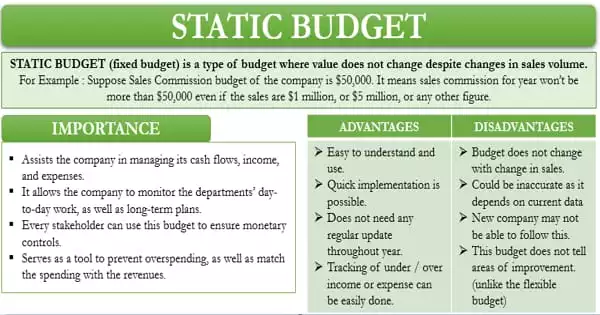

Static Budget Definition, Limitations, vs. a Flexible Budget

Steps to Prepare a flexible budget: 1. A comparison of actual performance to budgeted targets is pointless. Variable costs: The volume of activity has a direct and proportional effect on variable expenses. For one, a fixed budget is static, while a flexible budget is dynamic. One significant disadvantage of using a fixed budget is that it does not account for changes in expenditure and income over time. There are two kinds of budgets in Cost Accounting Cost accounting is a defined stream of managerial accounting used for ascertaining the overall cost of production.

Differences between fixed budget and flexible budget

This results in most fixed budgets lacking accuracy. Introducing flexibility can create confusion and break you from healthy patterns. For example, A business in the fashion industry has a flexible budget as fashion styles change frequently. This means that it will change according to the changes in the level of activity. For example, a seasonal business might create a flexible budget that anticipates changing staff levels as customers come and go over the course of the year. The purpose of the flexible budget is to allow better comparisons with the actual results by assessing them against the actual activity level Activity Level Master budget is prepared for a single activity level since is a static budget.

Difference Between Fixed Budget And Flexible Budget(With Table)

Determine the cost behaviour — fixed, variable, and semi-variable to each element of cost 4. Each element of cost is analysed according to its behaviour, i. It is difficult to establish effective control when a flexible budget is being used. On the other hand, a flexible budget is more complex. Zero-based budgeting is basically starting from zero on each budget, and then justifying all relevant needs and costs for the new budget.

Difference Between Fixed and Flexible Budget (Top 9)

This can be good for businesses that have predictable income and expenses. As previously indicated, both budget categories are significant in particular contexts. This discrepancy is likely to further increase over time. In this case, the company could use its flexible budget plan to increase spending on labor and equipment immediately instead of waiting for the next fiscal year. Semi-variable costs: Once costs are segregated, the budgeted costs would be computed for each level of activity.

Difference Between Fixed Budget and Flexible Budget (with Comparison Chart)

Your budget determines how much money you can spend on each aspect of your business and ultimately dictates your business's plan of action. As a result, it is referred to as a rigid or inflexible budget. This relates to a lack of budgeting function control. On the other hand, a flexible budget can be adjusted according to the business needs. A flexible budget continually bends with changes in the cost of a company, unlike a static budget.

Difference Between Fixed Budget And Flexible Budget With Comparison Chart

In this article, we will be taking a close look at two certain types of budgets: fixed budget, and flexible budget. Here are some of the major differences between the two: Nature A fixed budget is static by nature. Conversely, the Flexible budget is elastic because it can be easily adjusted according to the volume of the production. These budgets generally feature different rates per unit rather than a constant number, allowing an enterprise to foresee possible increases or drops in monetary requirements. Zero-Based Budgeting Zero-based budgeting is basically starting from zero on each budget, and then justifying all relevant needs and costs for the new budget. This represents your best guess at what will be spent and what will be earned. During the establishment of the fixed budget, the existing conditions are supposed not to change soon, and that is false.