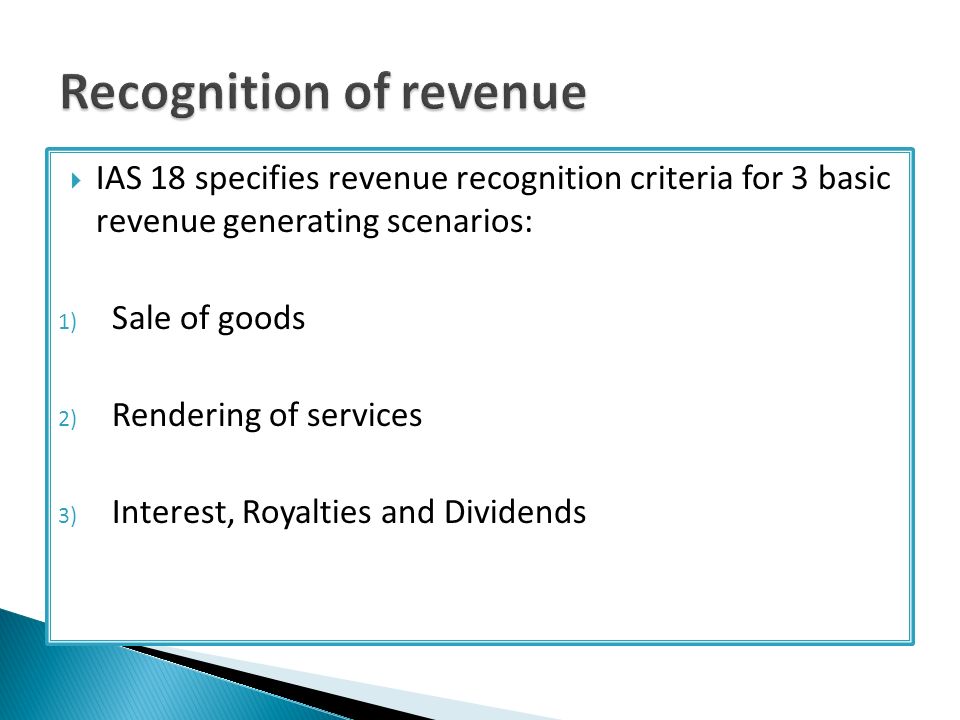

IAS 18, "Revenue," is an international accounting standard that provides guidance on the recognition of revenue from the sale of goods, rendering of services, and other activities. One of the key principles of IAS 18 is that revenue should be recognized when it is probable that the economic benefits associated with the transaction will flow to the entity and when the revenue can be reliably measured.

The recognition of expenses, on the other hand, is governed by the matching principle, which states that expenses should be recognized in the same period as the revenue they helped to generate. This means that expenses should be recorded at the same time as the revenue they relate to, rather than when they are incurred.

For example, if a company sells goods on credit, it will recognize the revenue when the goods are delivered to the customer, even if the customer has not yet paid for the goods. At the same time, the company will also recognize the related expenses, such as the cost of goods sold and any selling and administrative expenses incurred in the process of making the sale.

IAS 18 also specifies the conditions under which revenue should be recognized for the rendering of services. For example, revenue from a service contract should be recognized as the services are performed, rather than when the contract is signed or when payment is received.

In addition to the principles of revenue and expense recognition outlined above, IAS 18 also provides guidance on the recognition of revenue from the sale of assets and from construction contracts.

Overall, the goal of IAS 18 is to ensure that an entity's financial statements provide a fair and accurate representation of its financial performance and position. By following the guidance provided in this standard, entities can ensure that their revenues and expenses are recognized in a consistent and transparent manner, providing useful information to stakeholders about the entity's financial performance.