International convergence of accounting standards. International Convergence Of Accounting Standards 2022-12-11

International convergence of accounting standards Rating:

6,6/10

1879

reviews

The primary goal is the ultimate aim or objective that a person or organization strives to achieve. It is the main focus or driving force that guides the actions and decisions of an individual or group. The primary goal is often the end result that a person or organization hopes to attain, and it shapes their priorities, values, and strategies.

For individuals, the primary goal may be personal in nature, such as achieving financial stability, finding happiness, or pursuing a particular career or educational path. For organizations, the primary goal may be related to business objectives, such as increasing profits, expanding market share, or improving customer satisfaction.

The primary goal is often accompanied by secondary or tertiary goals, which are smaller or lesser objectives that support the achievement of the primary goal. These goals may be necessary steps or milestones along the way to achieving the primary goal, and they can help to keep an individual or organization focused and motivated.

Achieving the primary goal requires effort, dedication, and a clear plan of action. It may involve overcoming challenges, making sacrifices, and adapting to change. However, the sense of accomplishment and fulfillment that comes from achieving the primary goal can be well worth the journey.

In conclusion, the primary goal is the ultimate aim or objective that a person or organization strives to achieve. It shapes priorities, values, and strategies, and it requires effort, dedication, and a clear plan of action to achieve. Whether it is personal or business-related, the primary goal is the driving force that guides the actions and decisions of an individual or group, and it can bring a sense of accomplishment and fulfillment when achieved.

Convergence of Accounting Standards

Investors and creditors are skeptic to invest or lend money in corporations that operate on transnational markets without a good understanding of their financial positions. In this essay, I am going to evaluate the challenge of convergence, why it is necessary and the benefit it brings back for an economy. Those priority undertakings include joint undertakings on fiscal instruments, renting, gross acknowledgment, insurance contracts, just value measuring, and the presentation of other comprehensive income and the consolidation of investing companies. The Contentment combined the most common FIRS adoption approaches, Convergence and Endorsement. The United States, while comparable with a number of nations, contrasts greatly with the atmosphere and style of conducting business greatly distilled into the roots of foreign nations. It is surprising to hear that they are the biggest proponents for this.

International Convergence of Financial Reporting Flashcards

And the IASB engages with stakeholders closely all over the world, which includes investors, business leaders, regulators, analysts, accounting standard-setters as well as the accountancy profession. The aim of this paper is to review and comment the evolution and the major changes occurred in accounting for business combinations and for goodwill and their current status in the light of the process of convergence of accounting standards on these crucial economic transactions. The Investors Hanif and Mukherjee 2009 expounded that investors could be stated as the party most benefited by the convergence and they are the people to put money into different companies or markets. In recent times, significant progress has been made towards achieving one set of universally accepted financial reporting standards. International and even local standard setting bodies have come up with projects of harmonization and in most of the cases became successful. About 450 foreign companies in a variety of industries currently use IFRS for their SEC filings.

Convergence of International and US Accounting Principles and IFRS

The FASB has a batch of work to carry through with the IASB in doing this undertaking successful. Ernst and Young 2012 suggested, the convergence can better in term of instruction and preparation, so before doing a concluding determination to travel towards IFRS, the SEC can see the province of readiness of US issuers, hearers and users including the extent and handiness of IFRS instruction and preparation. Tax code and reporting regulations contain much greater depth and specificity than what is provided by FIRS. Comparability -IASB and FASB will work on existing frameworks to provide basis for developing future standards by boards Phases of project: -Objectives and qualitative characteristics -Elements and recognition -Measurement -Reporting entity -Presentation and disclosure -Purpose and status -Application to not-for-profits -Finalization Evidence of support for IFRS: -Adoption by the EU - public companies in the EU were required to begin using IFRS in 2005 -IOSCO has endorsed IFRS for cross-listings -IFAC G20 accountancy summit in July 2009 issued renewed mandate for adoption of global accounting standards -Latest IFAC Global Leadership Survey—emphasized that investors and consumers deserve simpler and more useful information -Adoption of IFRS in 2011: Japan, Canada, India, Brazil and Korea The complicated nature of standards such as financial instruments and fair value accounting The tax-driven nature of the national accounting regime Disagreement with significant IFRS, such as financial statements and fair value accounting Insufficient guidance on first time application of IFRS Limited capital markets are less beneficial Investor satisfaction with national accounting standards IFRS difficulties in language translation IASB's and FASB's key initiatives in the Norwalk Agreement in 2002: 1. CreditPulse: Yesterday you mentioned China in discussing IFRS.

Convergence potential - FASB assesses agenda items for possible cooperation with IASB. Convergence turned out to be more difficult than anticipated. Standards must be applied consistently and enforcement must be uniform, otherwise, a single set of standards may appear to exist but will lack desirable attributes such as comparability. The reporting for the segments also differs in the case of the standards. That's going to be an eye-opener for a lot of people. In 2007, the SEC began permitting foreign registrants to fully incorporate FIRS when filing their financial statements, without needing to reconcile them to GAP, a huge victory and step forward for the SAAB. What assurance will investors have that that same level of accountability will exist under IFRS? The effects of globalisation are manifested through the alterations in people 's civilizations, prosperity and economic development, alterations in political systems, societies and besides alterations in the environment.

Standards Convergence: The Movement Toward International Accounting Standards

In October last twelvemonth the boards published paperss seeking positions on ways to cut down the costs of using new demands, concentrating on the possible effectual day of the months and passage and whether early acceptance should be permitted. It could, however, make sense in industries with global players that adhere to IFRS. The FASB issues an Accounting Standards Update to inform people about changes to the FASB Codification, which includes changes to non-authoritative SEC content. Current accounting and reporting practices fall short of meeting the information needs of the capital markets in the 21st century. The Norwalk Agreement: The FASB and IASB Agree to Collaborate In September 2002, the FASB and the IASB met jointly and agreed to work together to better and meet U.

International Convergence Of Accounting Standards Accounting Essay Example

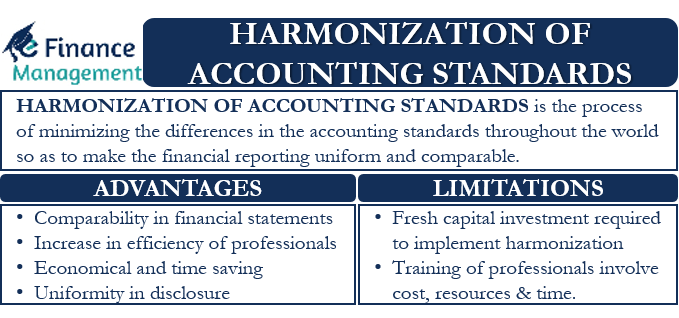

Therefore, it must eliminate the gap between the International Financial Reporting Standards IFRS and US Generally Accepted Accounting Principles GAAP. As mentioned, comprehensive FIRS training for staff members can be a costly investment engendering the uncertainty surrounding the issue. Assets held for disposal ADVERTISEMENTS: c. At their meeting in April, the boards agreed that they will pass extra clip beyond June 2011 to finish this joint work. Convergence among national and international accounting standards would foster comparability with the use of internationally converged accounting standards. At first the idea was to harmonize or converge the different accounting rules in different countries and make them better reflect one another. Another benefit that International Accounting houses could obtain with respects to the harmonisation of accounting patterns will be the decreased disbursals that they normally incur for motion of staff across national boundaries.

Process Of International Convergence Of Accounting Standards Accounting Essay

A inquiry on quality may originate in fortunes where the International Accounting Standards Board IASB , the organisation with the authorization of coming up with a consonant IAS, find it hard to hold consentaneous understanding on some of the accounting criterions. For example, if an organization is implementing a new software system, it should ensure that the new system is compatible with 'FURS. Companies in the United States and throughout the world now understand why having strong internal controls over financial reporting is important. Impairment recognition write-down to fair values d. It is funded by contributions from major accounting firms, private financial institutions and industrial companies, central and development banks, national funding regimes, and other international and professional organizations throughout the world.

Engaging in a high-level assessment of current operations and financial reporting using FIRS will benefit a company. The SEC was tasked to do a determination in 2011 on whether and how to integrate the IFRS in the United States but this unmeasurable determination was delayed. Basics, 2012 US GAP classifies assets and liabilities based on their nature by either current or non- current. . Understandability: Understandable to people with reasonable financial knowledge 2.

Recent accounting standards have moved off-balance-sheet items onto the balance sheet. Investors will first need to re-educate themselves on the newly recognized standards, but will then be able to more fluently analyze and evaluate reports. Eventually, the boards focused primarily on four specific joint projects: revenue recognition, insurance, financial instruments, and leases. Resolution on a wide variety of issues may be extremely difficult across the board. The boards also diverge on other major lease issues, most notably the recognition of expenses on the income statement. With globalisation we have witnessed an increasing volume of trade in goods and services and capital flows as foreign direct investings Levin Institute para1.

The International Convergence of Accounting Standards Essay Example

Fourth: Convergence means interaction between different states, between single states and the IASB, and between the IASB and regional professional accounting organic structures. Pounder: It is surprising to a lot of people. Having this done, they now focus on the risks and manage them efficiently. Although we have gone into great depth, the differences between the two sides are plentiful, as many issues have yet to be discussed on any level by professionals. They have a series of provincial securities regulators, they do not have a national securities regulator. In addition, the accounting information system promotes the activity of the enterprise effectively by preparing up-to-date information statements, providing as much information as possible so that the data should be understandable all users not only for the experts bookkeepers and tracking liquidity.