Research and development accounting treatment. 8.3 Research and development costs 2022-12-10

Research and development accounting treatment Rating:

8,8/10

529

reviews

Diary of a Mad Black Woman is a 2005 romantic drama film that tells the story of Helen McCarter, a successful lawyer whose perfect life is turned upside down when her husband, Charles, reveals that he is leaving her for another woman. After being thrown out of her home, Helen moves in with her estranged grandmother, Madea, who helps her rediscover her strength and inner resilience.

The film follows Helen as she navigates the ups and downs of her newfound single life, including dealing with the betrayal of her husband, navigating the dating scene, and rebuilding her career. Along the way, she receives guidance and support from her loved ones, including her grandmother, her mother, and her brother.

At its core, Diary of a Mad Black Woman is a story about self-discovery and empowerment. Through her journey, Helen learns to stand up for herself and to trust in her own abilities. She also learns the value of forgiveness and the importance of maintaining strong relationships with those she loves.

One of the standout features of the film is its portrayal of Madea, a larger-than-life character played by actor Tyler Perry. Madea is a wise and feisty grandmother who isn't afraid to speak her mind and who serves as a source of strength and guidance for Helen.

Overall, Diary of a Mad Black Woman is a heartwarming and uplifting film that celebrates the resilience and strength of the human spirit. It offers a message of hope and empowerment, and serves as a reminder that no matter how difficult life may seem, we all have the power to overcome challenges and emerge stronger on the other side.

Accounting Treatment of Research and Development Costs

To capitalize and estimate the value of these assets, an analyst needs to estimate how many years a product or technology will generate benefit for its economic life and use that as an assumption for the amortization period. If a company such as Intel or Bristol-Myers Squibb spends billions on research and development each year, what accounting is appropriate? The lives of many assets are determined by technological change. The Internal Revenue Service tax policy in the 1920s and 1930s favored the deferral treatment of research and development costs. GAAP, what reporting is appropriate for the cost of these two projects? Forty-four percent of these projects were technically successful, and only 16 percent were technically unsuccessful. However, it does not provide the possible applications of concepts or phenomena in production.

Accounting recognition of research and development expenditures in IAS 38

Cost recovery is the ability of businesses to recover deduct the costs of their investments. Tax Foundation, Tax Features March 1990 : 6. The managers will aim by consequence to avoid these restrictions. Therefore market research and testing—which are essentially about selling—are defined as marketing costs, which are expensed in the same period as the activities took place. Interest-ingly, in 1954 Congress merely removed the tax-financial ac-counting conformity requirement. Costs incurred in the research stage are expensed through the Statement of comprehensive income. A good quality of audit reflects usually a weaker earnings management Ben Othmen and al.

At approximately the same time other institutions, such as the National Association of Cost Accountants, promoted the same deferral treatment. The impact of SFAS No. The percentages associated with the likelihood of receiving a patent and generating future revenues are ignored. Research and development are applied across different industries and sectors. However, whether success is 100 percent likely or only 2 percent, no asset are reported on the balance sheet for these costs.

No one should act upon such information without appropriate professional advice after a thorough examination of the particular situation. This equipment should be capitalized as an asset and depreciated over its useful life. If development costs meet the rigid criteria specified in SSAP No. The investigation also revealed 60 percent of the companies disclosed the dollar amount of research and development in some way, but only 10 percent disclosed the accounting treatment in published financial statements. GAAP prefers not to address the uncertainty inherent in research and development programs but rather to focus on comparability of amounts spent between years and between companies.

Agreeing with the positive accounting theory, the political visibility is often correlated with the political costs Watts and Zimmerman, 1986. Under IFRS rules, research spending is treated as an expense each year, just as with GAAP. Therefore, the accounting treatment for all research expenditure is to write it off to the profit and loss account as incurred. Is there an Accounting Guide for the pharmaceutical industry? In our experience, the key factor in the above list is technical feasibility. As can be seen with Intel and Bristol-Myers Squibb, such costs are often massive because of the importance of new ideas and products to the future of many organizations.

Accounting Treatment Of Research And Development R D Accounting Essay

However, the impact of audit quality on levels of discretionary manipulation of managers, particularly in their accounting practices for intangible investments is very important, auditors with high audit quality encourage firms audited by them to communicate their intangible expenditure to preserve their reputation Bourmont, 2006. The assets would be subject to impairment testing under PPE Corp manufactures GPS technology products for use on golf courses. According to the Financial Accounting Standards Board, or FASB, generally accepted accounting principles, or GAAP, require that most research and development costs be expensed in the current period. This difference gives rise to two complexities in applying IFRS: distinguishing development activities from research activities, and analyzing whether and when the criteria for capitalizing development expenditures are met. Development is the translation of research findings or other knowledge into a plan or design for a new product or process or for a significant improvement to an existing product or process whether intended for sale or use. Because success is highly uncertain, accounting has long faced the challenge of determining whether such costs should be capitalized or expensed.

What is the purpose of the pharmaceutical industry research credit Audit Guidelines? Interpretation of the matching principle gets a bit fuzzy when dealing with research and development. BETA: is a sensitivity coefficient of the assets returns to the market returns. As a result, IAS 38 states that allexpenditure incurred at the research stageshould be written off to the income statementas an expense when incurred, and will never be capitalised as an intangible asset. The outcome is uncertain, but the money was spent under the assumption that future economic benefits would be derived. GAAP requires that all research and development expenditures must be expensed as incurred. As a result, fewer transactions are expected to involve acquiring or selling a business. LIST-US: a dummy variable that takes the value 1 if the company is listed on a U.

Funding is paid directly from the Investor Co. Thus, accounting organizations had generally supported the deferral treatment for research and development expenditures. All costs are expensed. Typically, the pharmaceutical company departments involved in this stage of the drug development process are pharmaceutical development, analytical chemistry, biostatics, pharmaceutical technology development, drug safety, toxicology, and clinical research and development. The first motivation concerns the debt-covenant, the second incentive is to reduce the variability of results by the management to increase or decrease profits in order to minimize the risk taken by investors: we speak in this case about earnings smoothing, the third motivation concerns the reduction of political costs, and finally the bonus plans. SUMMARY Since research and development expenditures are signifi-cant in amount, the historical accounting treatment of this im-portant cost was investigated. All Answers ltd, 'Accounting Treatment Of Research And Development R D Accounting Essay' UKEssays.

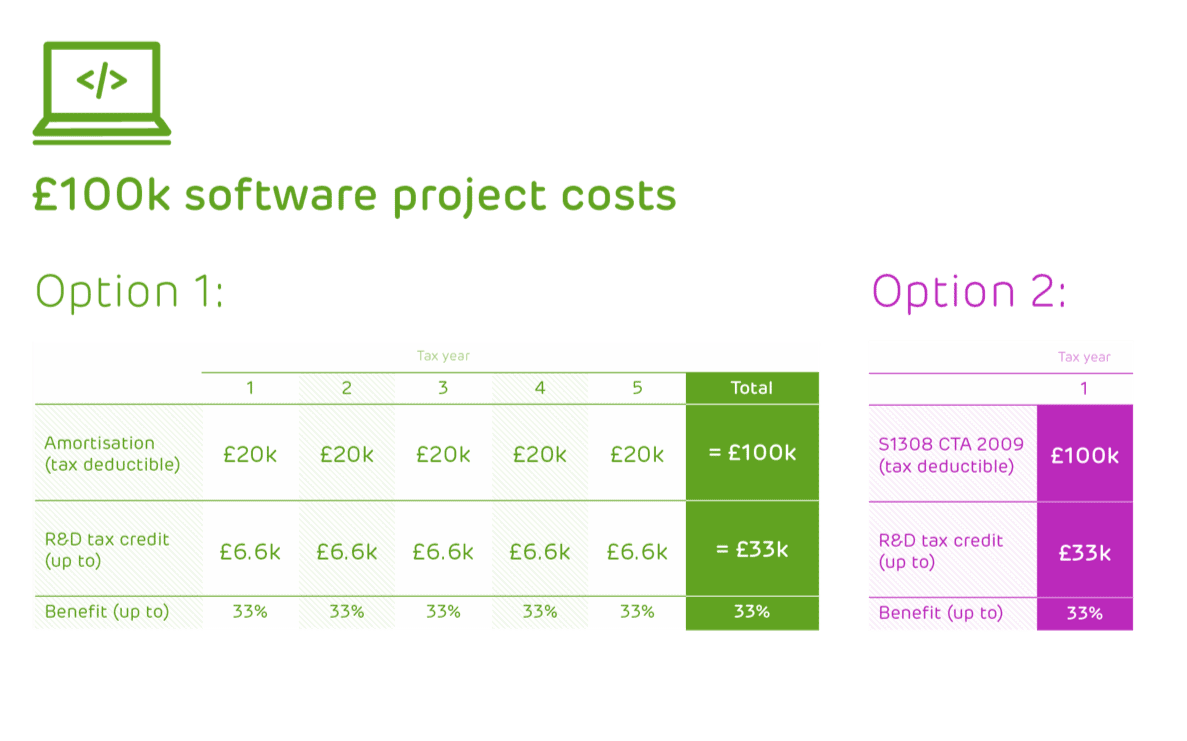

Accounting treatment of software development costs

Previously working on the federal team as an intern in the summer of 2018 and as a research assistant in summer 2020. The company is researching theunknown, and therefore, at this early stage,no future economic benefit can be expected toflow to the entity. The IASB expects to complete its discussions in the first half of 2018. Pharma Corp enters into a contract with Research Corp, a third-party professional research organization, to perform research activities for a period of three years in connection with a drug compound for a cancer treatment. Furthermore, the impact of SFAS No. However, the tax law prior to 1954 allowed the current expensing of research and development only when the same procedure was followed in the financial statement.