Right of return revenue recognition. FASB ASU 2018 2022-12-12

Right of return revenue recognition Rating:

9,6/10

1481

reviews

Technology has become an integral part of our daily lives. From the smartphones in our pockets to the computers on our desks, technology has revolutionized the way we communicate, work, and access information.

One of the major benefits of technology is the way it has connected us globally. With the internet and social media, we can connect with people across the world and share ideas, opinions, and experiences. This has led to a more connected and informed global community.

Technology has also changed the way we work. With the advent of laptops and cloud computing, we can now work from anywhere and at any time. This has led to a rise in remote work and the gig economy, giving people more flexibility in their careers and allowing them to pursue their passions and interests.

In addition, technology has made it easier for people to access information and learn new things. With the internet and online educational resources, we can learn about any topic at any time and from any location. This has opened up new opportunities for learning and personal growth.

However, technology also has its drawbacks. One major concern is the issue of privacy. With the amount of personal information we share online, there is a risk of data breaches and identity theft. In addition, the increasing reliance on technology has led to a decrease in face-to-face communication and a rise in screen time, which can have negative impacts on mental health and social skills.

Overall, technology has brought about many positive changes in our lives, but it is important to use it responsibly and consider the potential negative impacts. It is up to us as individuals and as a society to find a balance and use technology in a way that benefits us and the world around us.

Revenue Recognition Applied: Manufacturing & Distribution

This article was originally published on June 22, 2018. A refund liability, presented separately from the associated refund asset, should be recognized for those goods expected to be returned. But for many, the current mindset is that the government does not give contributions — that way of thinking equates the benefits received by the general public to the government receiving commensurate value in return for the assets transferred. Most accountants agree that financial statements should reflect the sub-stance of a transaction, and not merely its legal form. There are various reasons for this, but one is that such an approach treats unexpired customer rights of return, where they exist, as the main driver of revenue recognition, irrespective of how significant - or insignificant - such rights are so far as the buyer and seller are concerned. Implied rights can arise from statements or promises made to customers during the sales process, statutory requirements, or a reporting entity's customary business practice.

Revenue Recognition: What It Means in Accounting and the 5 Steps

Contracts must identify all parties usually your company and your client , the rights of each party and the payment terms. These provisions are commonly included in situations when an award is made based upon the qualifications of a particular individual. In some instances, determining that objective customer acceptance rights have been met is a formality because the entity has sufficient experience with similar products being accepted according to the objective criteria in the contract. For example, a resource provider might stipulate that a recipient must achieve performance levels or goals that are measurable in terms of specified outputs, outcomes, or levels of service. For example, if a company cannot reliably estimate the future warranty costs on a specific product, the criteria are not met. For example, the sale of a car with a complementary driving lesson would be considered as two performance obligations — the first being the car itself and the second being the driving lesson.

How to recognize revenue when rights of return are present

It should be noted that a benefit provided to the general public does not constitute commensurate value to the resource provider. A refund asset should be recognized to reflect the actual value of the goods expected to be returned after considering any expected reduction in the value of the returned goods. This can be calculated using one of two methods 1 the expected value or 2 the most likely amount. We use cookies to personalize content and to provide you with an improved user experience. For goods that are expected to be returned, the amount the reporting entity expects to repay its customers that is, the estimated refund liability is the consideration paid for the goods less the restocking fee. One of the most common forms of grants we see where commensurate value exists are when payments are being made on behalf of third parties, for example, a payment from Medicare, Medicaid, or another state agency where the agency is covering the cost of care to a specified individual. Distributor has the right to return the video games for a full refund for any reason within 180 days of purchase.

It may initially seem surprising that a seller would allow a customer to determine what to pay - won't the customer want to pay as little as possible? This gives rise to an issue: how should the amount of revenue be measured? Rights of return affect the total transaction price to be allocated among the performance obligations in step three, while customer acceptance rights change the determination of when control actually transfers to the customer in step five. One exception to this is if cash or other assets were received in advance. This averages roughly 200 meals per week. All other entities should apply the amendments for transactions in which the entity serves as the resource provider, to annual periods beginning after December 15, 2019, and interim periods within annual periods beginning after December 15, 2020. GAAP Revenue Recognition Principles The Financial Accounting Standards Board FASB which sets the standards for U. Is it enough to enable users to understand how you are accounting, or does it need to be enhanced? In other cases, the return privilege may last over an extended period of time, as in magazine and textbook publishing and equipment manufacturing. For reasons of space, the arguments are not reproduced here, but one particular aspect of the issue is worth flagging: what if the amount of revenue is determinable by the customer? CLA CliftonLarsonAllen LLP is not an agent of any other member of CLA Global Limited, cannot obligate any other member firm, and is liable only for its own acts or omissions and not those of any other member firm.

Vendor Y determines that it is probable that no significant revenue reversal will occur for this amount. To determine the transaction price for goods transferred, an entity should consider the effects of a right of return. Customer rights of return A further issue, somewhat related to that described above, arises with customer rights of return. If the former, the seller will recognise a sale on exchange, making provision for the expected level of returns; if the latter, a sale will be recognised only if and when you choose not to return the goods. As a result, the restocking fee should be included in the transaction price and recognized when control of the goods transfers to the customer. Estimates Each entity will have different promises related to their right of returns and, therefore, may require a different method of estimating.

If the performer involved has no track record, this may be less of a problem; the high degree of uncertainty will point to a low fair value for the song-writer's revenue. They are not subject to a probability or likelihood assessment. Revenue should not be recorded for the portion of the sale the entity expects to be returned. However, if the seller is unable to make a reasonable estimate of the amount of future product returns, the seller should wait to record revenue until the loss can be estimated or the return privilege expires. Vendor Y has significant historical experience with customers of this type, and expects an average of 3 percent of all widgets to be returned.

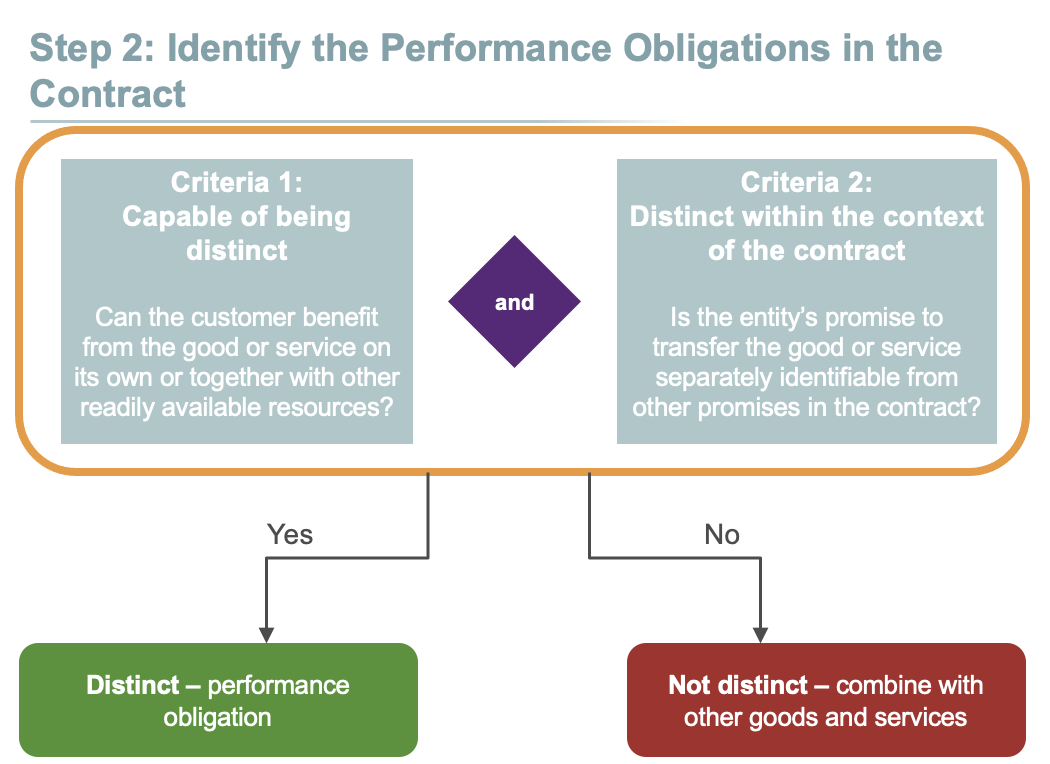

Performance obligations must be distinct from each other. Rights of Return As nonpublic companies are analyzing their contracts to ensure compliance with ASC 606 Revenue from Contracts with Customers, the internal accounting departments at these entities are having to gain a better understanding of what promises the sales departments are making to customers. Reporting on the project would not be a stipulation creating a barrier. Generally speaking, the earlier revenue is recognized, it is said to be more valuable to the company, yet a risk to reliability. Rights to receive uncertain amounts For the large majority of transactions, the amount of consideration that a seller will receive is fixed.

Rights of Return and Customer Acceptance in ASC 606

It prevents entities from recognizing sales revenue on transactions with parties that the sellers have established primarily for the purpose of recognizing such sales revenue. Milestones are also considered performance-related barriers, and gifts or grants involving milestones become unconditional in stages as each milestone is met No. Rights of Return ASC 606 requires that rights of return be treated as variable consideration. The COGS is 80%. To my mind, neither of these extremes is appropriate; the answer lies somewhere in between. Step two in the flowchart requires organizations to determine whether a contribution is conditional.

Another example would be a requirement that a matching amount of contributions would need to be obtained by an organization. It should be measured at the carrying amount of the goods at the time of sale, less any expected costs to recover the goods, including potential decreases in the value of the returned products. However, a real-life example should demonstrate the fallacy of this assumption. Where Applied does not have prior experience of meeting agreed-upon specifications for example, in cases of a new product with no history of meeting customer specifications , technical acceptance is considered a requirement before we conclude that the customer has obtained control, as described in ASC 606-10-55-87, and revenue is recognized. In either case, an unambiguous threshold for entitlement is established that will clearly indicate to both resource provider and resource recipient whether the threshold has been met and if so, when that occurred. The right of return should be estimated in the same way as other variable consideration under ASC 606.