State and local taxes are an important source of revenue for governments at the state and local level. They play a critical role in funding the various programs and services that are necessary for the well-being of communities and their citizens. In this essay, we will outline the various types of state and local taxes, discuss how they are collected, and consider some of the key issues surrounding these taxes.

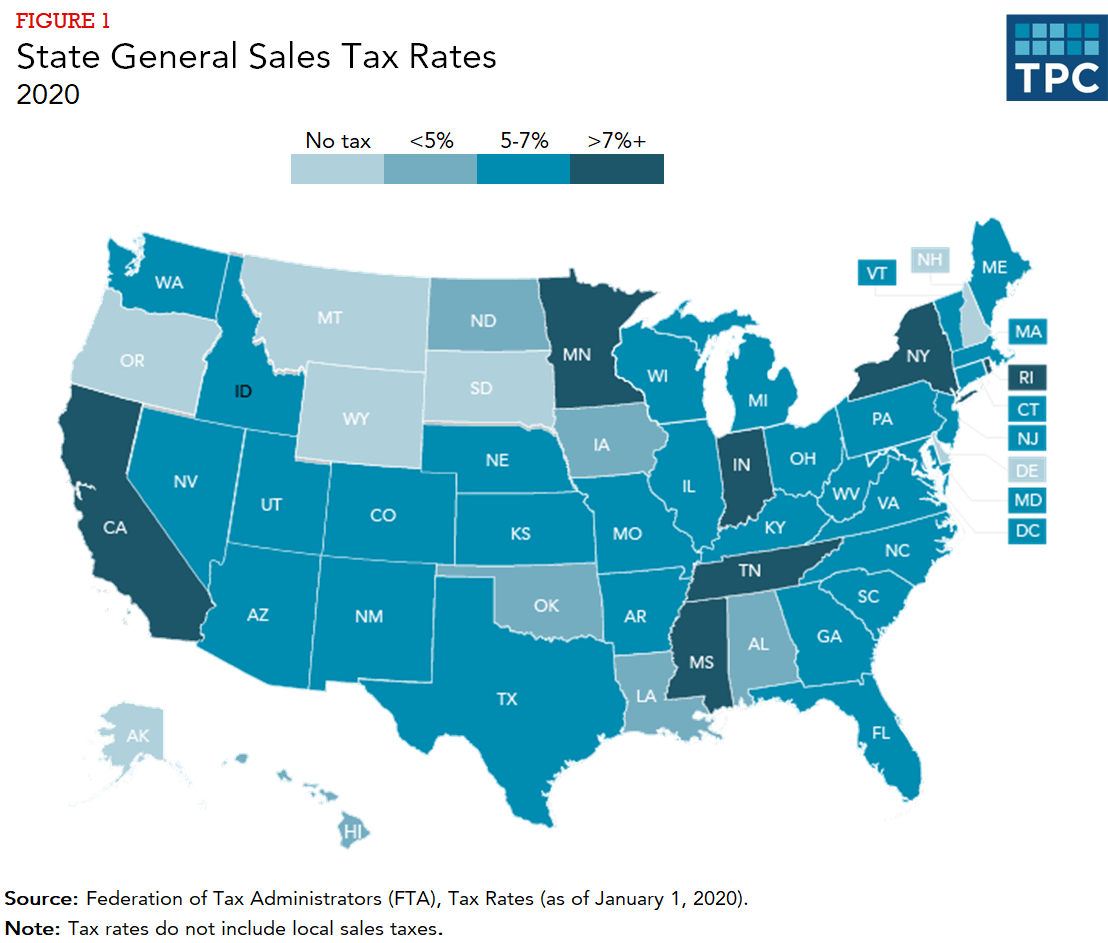

There are several different types of state and local taxes, including sales taxes, property taxes, and income taxes. Sales taxes are taxes that are levied on the sale of goods and services. These taxes are typically collected by merchants at the point of sale and are passed on to the state or local government. Sales taxes are typically based on the price of the goods or services being sold and are expressed as a percentage of the purchase price.

Property taxes are another common type of state and local tax. These taxes are levied on real estate and are typically based on the value of the property. Property taxes are usually collected by local governments and are used to fund schools, police and fire departments, and other public services.

Income taxes are also collected by many states and localities. These taxes are typically based on the amount of money that individuals or businesses earn, and are often progressive, meaning that higher earners pay a higher percentage of their income in taxes.

State and local taxes are typically collected in one of two ways. The first is through a tax return, which is a document that individuals or businesses are required to file each year in order to report their income and pay their taxes. The second way is through a withholding system, in which taxes are collected from paychecks or other sources of income throughout the year.

There are a number of issues surrounding state and local taxes that are worth considering. One key issue is the distribution of tax burdens across different income groups. Some argue that state and local taxes are disproportionately burdensome for lower-income individuals and families, while others argue that these taxes are necessary to fund important public services and programs.

Another issue is the potential for states and localities to engage in tax competition, in which they attempt to lure businesses and individuals to their jurisdiction by offering lower tax rates. This can lead to a "race to the bottom" in which governments cut taxes in an effort to attract new residents and businesses, potentially undermining the ability of states and localities to fund important public services.

In conclusion, state and local taxes are an important source of revenue for governments at the state and local level. These taxes fund the programs and services that are necessary for the well-being of communities and their citizens. There are several different types of state and local taxes, including sales taxes, property taxes, and income taxes. These taxes are collected through tax returns and withholding systems, and there are a number of important issues surrounding their distribution and potential impacts on economic growth.