Swiss gaap vs us gaap. Difference Entre Ifrs Us Gaap Swiss Gaap Fer 2023-01-07

Swiss gaap vs us gaap Rating:

7,6/10

237

reviews

Swiss GAAP and US GAAP are two different sets of accounting standards that are used to guide the preparation of financial statements. While both sets of standards have similar objectives, there are some key differences between the two that are important to understand.

One of the main differences between Swiss GAAP and US GAAP is the level of detail and complexity in the standards. Swiss GAAP tends to be less detailed and more flexible than US GAAP, which is known for its complexity and stringent requirements. This difference in approach is reflected in the way that financial statements are prepared and presented under each set of standards.

Another difference between Swiss GAAP and US GAAP is the level of discretion allowed in the application of the standards. Swiss GAAP allows for a greater degree of discretion in the interpretation and application of the standards, whereas US GAAP is more prescriptive in nature. This difference can have significant implications for companies operating in different countries and may require them to adopt different accounting practices.

A third difference between Swiss GAAP and US GAAP is the level of transparency required in financial reporting. US GAAP requires more detailed and transparent reporting, with a focus on providing investors and other stakeholders with a clear understanding of a company's financial position and performance. In contrast, Swiss GAAP allows for more flexibility in the presentation of financial information, which may not be as transparent.

Overall, it is important for companies to understand the differences between Swiss GAAP and US GAAP and to choose the set of standards that is most appropriate for their operations. While both sets of standards have their strengths and weaknesses, the choice of GAAP will depend on the specific needs and circumstances of the company.

Swiss GAAP FER conversion

Deferred tax on US GAAP-to local stat-to local tax differences should be recorded in US GAAP financials of foreign entity. We know the requirements and idiosyncrasies of your industry. Swiss GAAP FER Contingent liabilities need to be disclosed within the notes. The standards are issued by the Commission for Financial Reporting Standards on the basis of a broadly underpinned process in Switzerland. Currently, it is anticipated that the U.

Research and development costs Refers to expenses incurred for research and development to create innovative products and services; Research costs are expenses as incurred, and developmental costs are capitalized; GAAP requires both research and development costs to be expensed as incurred; Capitalization of interest costs During construction, certain costs are capitalized as part of asset costs. Such convergence requires that the functions of the GAAP standards be added to the IFRS. Of course there are many differences in language; however, we will review some major differences in accounting standards with respect to Equity accounts. The objective of an excellent financial reporting would be to provide sufficient financial information about the reporting entity such that it would tend to be useful for all the potential investors, lenders, stakeholders, creditors, etc. Reversal of impairment losses is required in certain circumstances, except for goodwill. Until then, it becomes crucial for an analyst to be cautious of such differences when attempting to decode and analyze financial reports. My analysis will focus on: The differences between IFRS and U.

Long-lived asset contributions are recorded as revenue in the period received. SEC registrants should follow SEC regulations. Industry-specific guidance applies to investor entities for example, investment entities. Unlike the IFRS, for example, the Swiss GAAP FER do not break down the statement of comprehensive income into comprehensive income and other comprehensive income OCI. Special rules apply with regard to the abolishment of the principal allocation and Swiss finance branch reliefs that were withdrawn by the Swiss Federal Tax Administration on 24 May 2019 with legal effect as of 1 January 2020.

This means that differences in the way comparable transactions are treated can hardly be avoided. Equity method required except in specific circumstances. Specific rules exist for acquired in-process research and development generally expensed. Termination indemnity schemes are accounted for as pension plans; related liability is calculated as either a vested benefit obligation or according to the actuarial present value of benefits. Those must include at least the major captions and subtotals that were reflected in the most recent annual financial statements. More than ever, they are accountable to growing numbers of active stakeholders — including governments and regulators across the world — for their approach to environmental, social and governance issues.

Local GAAP to US GAAP adjustments and deferred taxes

Amounts due under finance leases are recorded as a receivable. For more detail about the structure of the KPMG global organization please visit. Losses have to be recognised immediately. The notes need to disclose why the accounting principle has changed, the nature of the change and its financial impact. General recognition criteria apply also for restructuring provisions. This is driving changes in expectations about what information businesses need to provide in their annual reports and financial statements. Discontinued operations — presentation and main disclosures Not addressed.

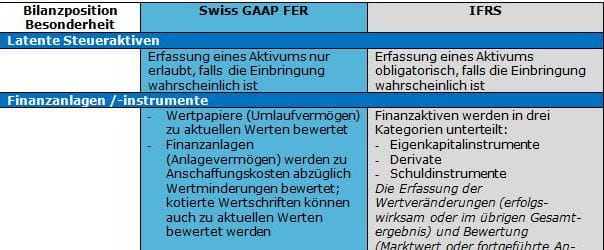

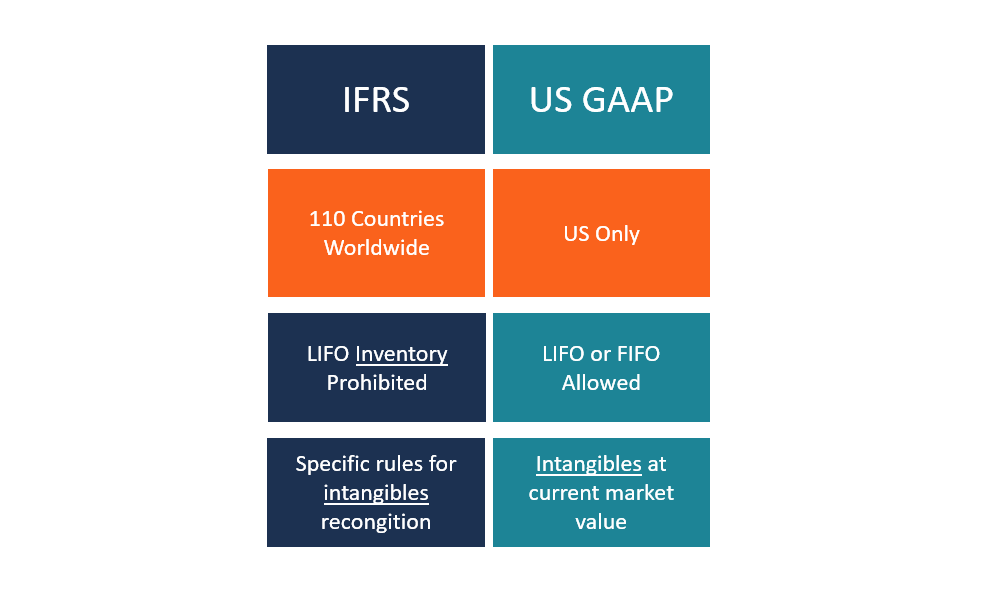

The main differences have to do with the presentation of financial statements, the treatment of goodwill in connection with business combinations, financial instruments and pension benefits. Additionally, the reporting entity is entitled to apply a lower tax rate — which is explicitly mentioned in the respective cantonal tax law — on a portion of its taxable profit during a period of up to five years. Difference Between IFRS and US GAAP The International Accounting and Standards Board IASB issues IFRS, whereas GAAP is issued by the Financial Accounting Standards Board FASB. If impairment is indicated, assets are written down to higher of fair value less costs to sell and value in use. Their extensive disclosure rules have recently come in for frequent criticism. This publication focuses on the measurement similarities and differences most commonly found in practice. US GAAP Similar to IFRS, but individually significant items are presented on the face of the income statement and disclosed in the notes.

Swiss GAAP FER also mention expenses which cannot be capitalised e. Certain minimum items are presented on the face of the balance sheet. Choosing the right one depends on the addressees and stakeholders of the financial reporting. The meeting covered a broad range of topics, including the future relationships between the IASB and regional and national standard setters, topical issues in financial reporting, reports from regional groups and administrative matters. A detailed report of proceedings at the meeting has now been released, outlining discussions on numerous topics such as the relationship between standard setters and the IASB, the IASB's work programme and processes, and a report on the possible adoption of IFRS in the United States noting a possible "step back".

Swiss GAAP FER Not addressed. Swiss GAAP will not be permitted. Basis of reporting is similar to IFRS. This process keeps evaluations consistent in the company Work Plan,… U. Standard headings but limited guidance on contents.

Business combinations Types: acquisitions or mergers All business combinations are acquisitions, thus the purchase method is the only method of accounting that is allowed. Because national and regional jurisdictions are expected to build on that global baseline, this will impact all companies, including those reporting under IFRS Standards and US GAAP. Geographic market and business segment information necessary if business sectors differ significantly. Termination benefits Four types of termination benefits with three different timing methods for recognition. Furthermore, the IFRS carrying values are also not changing. Swiss GAAP FER has a modular structure core FER, full Swiss GAAP FER, listed companies , which makes it suitable for companies of different sizes.