Variable and absorption costing explaining operating income differences. Exercise 2022-12-26

Variable and absorption costing explaining operating income differences Rating:

5,7/10

172

reviews

Variable costing, also known as direct costing, is a method of costing that only includes the variable costs of production in the cost of goods sold (COGS) on the income statement. Variable costs are those that vary in direct proportion to the volume of production, such as the cost of raw materials and direct labor. Fixed costs, on the other hand, are those that do not vary with the volume of production and include expenses such as rent, insurance, and property taxes. Under variable costing, fixed costs are not included in the COGS and are instead treated as period costs and expensed in the period in which they are incurred.

Absorption costing, on the other hand, includes both variable and fixed costs in the COGS. This means that the full cost of producing a product, including both the direct and indirect costs, is recognized in the income statement. Indirect costs, also known as overhead, are those costs that cannot be directly traced to a specific product or unit of production and include expenses such as indirect materials and indirect labor.

The main difference between the two methods is how they treat fixed costs. Under variable costing, fixed costs are not included in the COGS and are expensed as they are incurred. This means that operating income is higher under variable costing because it does not include the fixed costs in the COGS. Under absorption costing, fixed costs are included in the COGS and are therefore recognized as an expense in the income statement. This results in a lower operating income compared to variable costing because the fixed costs are recognized as an expense in the income statement.

There are several factors to consider when choosing between the two methods. One of the main advantages of variable costing is that it provides a better indication of the contribution margin, which is the amount of revenue remaining after the variable costs have been subtracted. This can be useful for decision-making purposes, as it allows managers to see the impact of changes in volume on profitability. Additionally, variable costing is simpler to calculate and understand because it only includes the variable costs in the COGS.

However, absorption costing has several advantages as well. One of the main advantages is that it provides a more accurate representation of the true cost of production. By including both variable and fixed costs in the COGS, absorption costing recognizes the full cost of producing a product and provides a more accurate picture of the company's profitability. This can be useful for external reporting purposes, as it provides a more accurate representation of the company's financial performance.

In conclusion, variable and absorption costing are two different methods of costing that are used to calculate the cost of goods sold on the income statement. The main difference between the two methods is how they treat fixed costs, with variable costing expensing fixed costs as they are incurred and absorption costing including them in the COGS. Both methods have their own advantages and disadvantages and the choice between the two will depend on the specific needs and goals of the company.

Chapter 9 with blog.sigma-systems.com

With variable costing, only the variable costs or production are added to the cost of the product during the work in process phase, and the fixed costs are expensed in the period in which they are incurred. The budgeted level of production used to calculate the b per unit is 500 units. This is typically known as the deferring of fixed cost in the inventory. In this article, we define absorption and variable costing and list the significant differences between the two accounting methods. Reducing the final selling price will result in lower net income because fixed manufacturing overhead resides as a period cost on the income statement. Advantages and Disadvantages of the Variable Costing Method Variable costing only includes the product costs that vary with output, which typically include direct material, direct labor, and variable manufacturing overhead. Absorption costing is in accordance with GAAP, because the product cost includes fixed overhead.

Since absorption costing takes all the potential costs into accounts in the calculation of per unit cost, some people believe that it is the most effective method to calculate the unit cost. Therefore, the cost of a product under absorption costing consists of direct material, direct labour, variable manufacturing overhead, and a portion of a fixed manufacturing overhead absorbed using an appropriate base. There are two major methods in manufacturing firms for valuing work in process and finished goods inventory for financial accounting purposes: variable costing and absorption costing. Including all manufacturing overhead — fixed and variable — gives companies a more accurate description of costs needed to produce goods. Variable Costing January February March Sale 700 800 1500 Sale Value 2100000 2400000 4500000 Variable Costing: Variable COGS 630000 720000 1350000 Variable Marketing Cost 420000 480000 900000 Total Variable Expenses 1050000 1200000 2250000 Contribution Margin 1050000 1200000 2250000 Fixed Expenses Fixed Manufacturing OH 400000 400000 400000 Fixed Selling and Admin OH 140000 140000 140000 Total Fixed Expenses 540000 540000 540000 Net Operating Income Loss 510000 660000 1710000 Absorption Costing January February March Sale Value 2100000 2400000 4500000 Less: COGS 1030000 1120000 1750000 Manufacturing Variable Cost 630000 720000 1350000 Manufacturing Fixed Cost 400000 400000 400000 Gross Margin 1070000 1280000 2750000 Less: Selling and Marketing Expenses 560000 620000 1040000 Variable Marketing Expenses 420000 480000 900000 Fixed Marketing OH 140000 140000 140000 Net Operating Income Loss 510000 660000 1710000 Contribution Margin has changed because in Variable costing only variable cost pertains are recorded to derive the COGS whereas in Absorption costing COGS is composed of fixed as well as variable manufacturing cost. The management should look at consumer insights, relation with buyers, the effect on brand-building, and other factors while making decisions.

Causes of difference in net operating income under variable and absorption costing

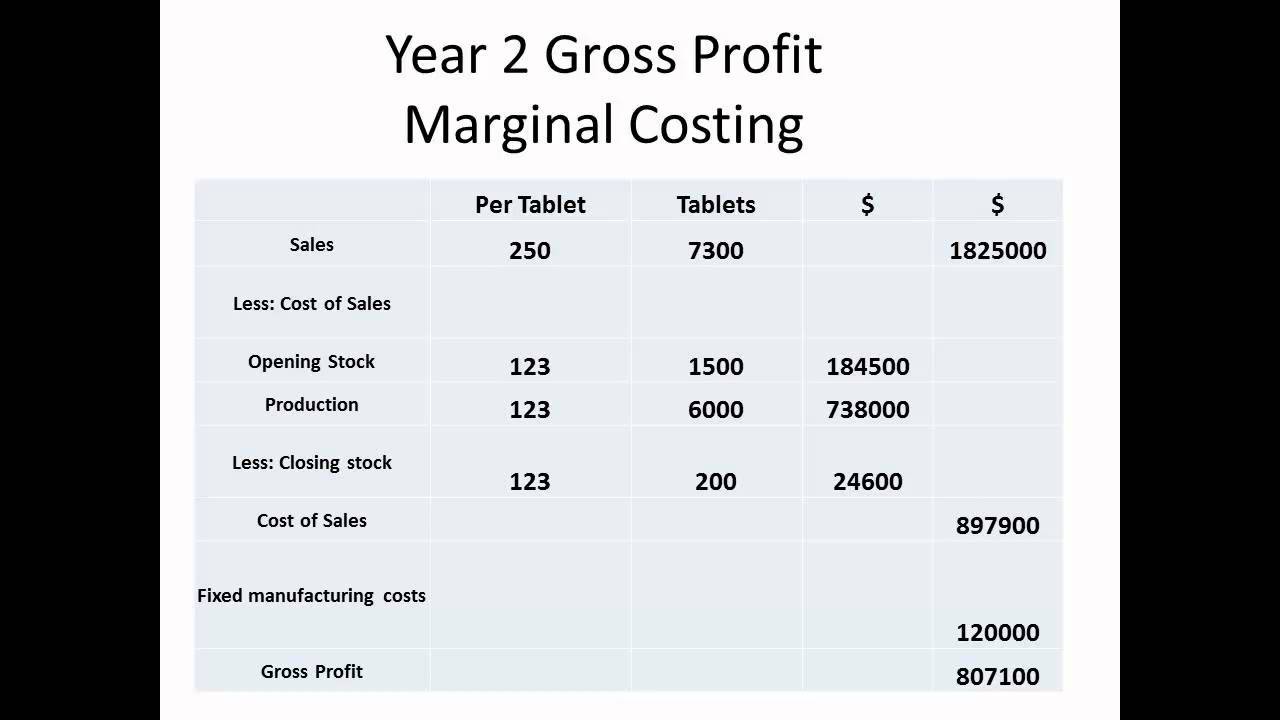

Absorption Costing Under absorption costing, all production costs direct labor, direct materials, and factory overhead whether fixed or variable are considered products costs. Sales xx Less: Cost of Sales xx Gross Profit xx Less: Selling and Administrative Expenses xx Operating Income xx Variable Costing Income Statement Variable or direct costing favors the contribution margin income statement format. This facilitates appraisal of the profitability of products, customers, and business segments. As a result, the net income under variable costing differs from absorption costing by the same amount as inventory differential. Inventories at the beginning and end of the year were as follows: Also, assume that 30% of the beginning and ending inventories were fixed costs. Using the absorption costing method can increase the inventory value, which may affect the gross profit and increase the price of products.

Difference Between Absorption Costing and Variable Costing

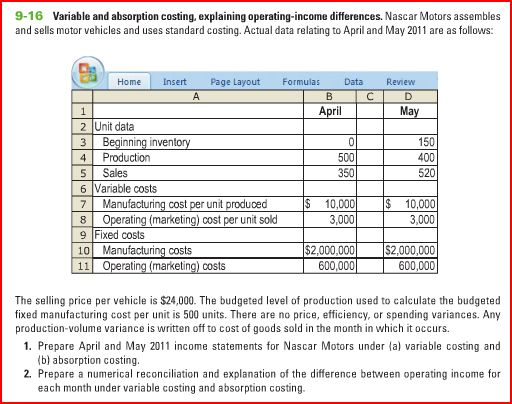

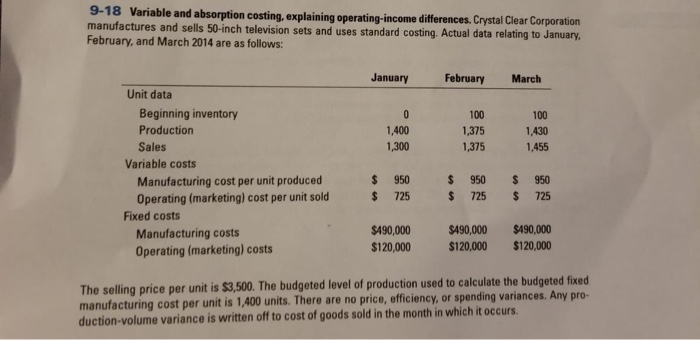

In variable costing, cost of the product is lower than the cost calculated under absorption costing. Under this method, all the fixed and variable production costs are deducted, and then fixed and variable selling expenses are deducted. Managerial decisions may also be different under each method. Prepare April and May 2017 income statements for Nascar Motors under a variable costing and b absorption costing. Any production- volume variance is written off to cost of goods sold in the month in which it occurs.

6.5 Compare and Contrast Variable and Absorption Costing

The formula for the break-even analysis requires calculating both the fixed costs and the variable costs of the product's manufacturing. In contrast, variable costing considers mere direct variable costs as product cost. There are no price, efficiency, or spending variances. When a company sells more than it produces during the current period, this indicates it is selling goods produced in a prior period. With absorption costing, all manufacturing costs are captured in the finished goods inventory account, and as those goods are sold, those costs become expenses. Income Comparison of Variable and Absorption Costing: The income statements prepared under absorption costing and variable costing usually produce different net operating income figures.

Variable and absorption costing, explaining operating

This will result in net income under variable costing being greater than under absorption costing. One issue, for example, is to select which method provides the most accurate product cost and meets accounting guidelines. Companies that use variable costing may be able to allocate high monthly direct, fixed costs to operating expenses. Prepare an income statement using a variable costing and b absorption costing. Therefore, managers must determine which method their company should use. Tyva is preparing its budget for June 2018 and has estimated sales based on past experience. Gross margins are not distorted by the allocation of common fixed costs.

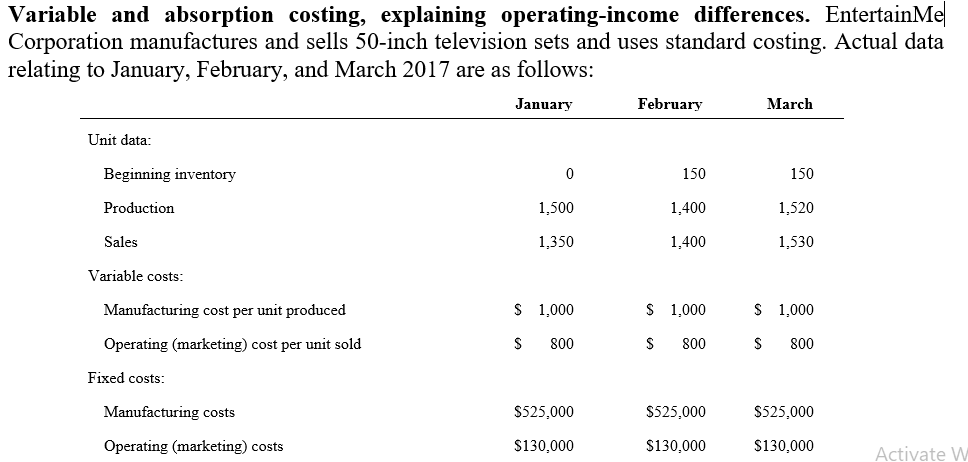

Any production-volume variance is written off to COGS in the month in which it occurs. Variable costing is an accounting method for production expenses where only variable costs are included in the product cost. Prepare income statements for EntertainMe in January, February, and March 2017 under a variable costing and b absorption costing. Any production-volume variance is written off to COGS in the month in which it occurs. On April 30, the end of the first month of operations, Joplin Company prepared the following income statement, based on the absorption costing concept: If the fixed manufacturing costs were 450,000 and the fixed selling and administrative expenses were 165,000, prepare an income statement according to the variable costing concept.

+table.JPG)

:max_bytes(150000):strip_icc()/dotdash-INV-final-Absorption-Costing-May-2021-01-bcb4092dc6044f51b926837f0a9086a6.jpg)