WorldCom was once one of the largest telecommunications companies in the world, with a market value of over $180 billion at its peak. However, in 2002, the company was at the center of one of the biggest accounting scandals in history, which ultimately led to its bankruptcy and the loss of billions of dollars for investors.

The scandal at WorldCom began to unravel in 2002 when Scott Sullivan, the company's chief financial officer, was fired for undisclosed reasons. After his departure, it was discovered that Sullivan had been directing the company's accounting department to manipulate the financial statements in order to make it appear as though the company was performing much better than it actually was.

One of the main ways that Sullivan and his accomplices at WorldCom were able to manipulate the financial statements was by booking expenses as investments. This allowed the company to inflate its profits and make it appear as though it was growing more rapidly than it actually was.

In addition to booking expenses as investments, WorldCom also engaged in a practice known as "cookie jar" accounting. This involved setting aside reserves of money in good years, which could then be used to offset losses in bad years. This allowed the company to smooth out its financial results and make it appear as though it was consistently profitable.

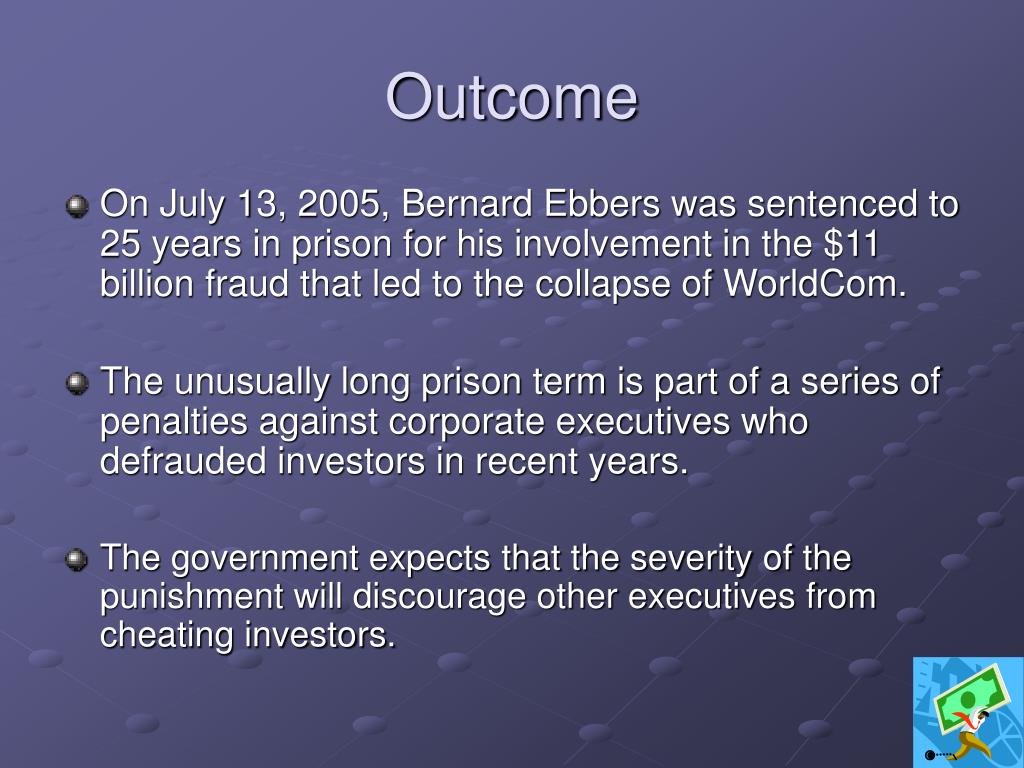

As the scandal at WorldCom began to come to light, the company's stock price plummeted and investors lost billions of dollars. In the end, WorldCom was forced to file for bankruptcy, and several top executives, including Sullivan, were sentenced to prison for their role in the fraud.

The WorldCom scandal had far-reaching consequences, not just for the company itself, but for the entire accounting industry. It led to greater scrutiny of corporate financial statements and increased regulation of accounting practices, as well as a loss of trust in corporate leadership.

Overall, the WorldCom scandal serves as a cautionary tale about the dangers of corporate greed and the importance of ethical business practices. It is a reminder that companies must be transparent and accountable in their financial reporting, and that those who engage in fraudulent activity will ultimately be held accountable for their actions.