Eisner v macomber. TaxConnectionsMoments In Tax History: Income, An Origin Story 2022-12-23

Eisner v macomber Rating:

9,3/10

1571

reviews

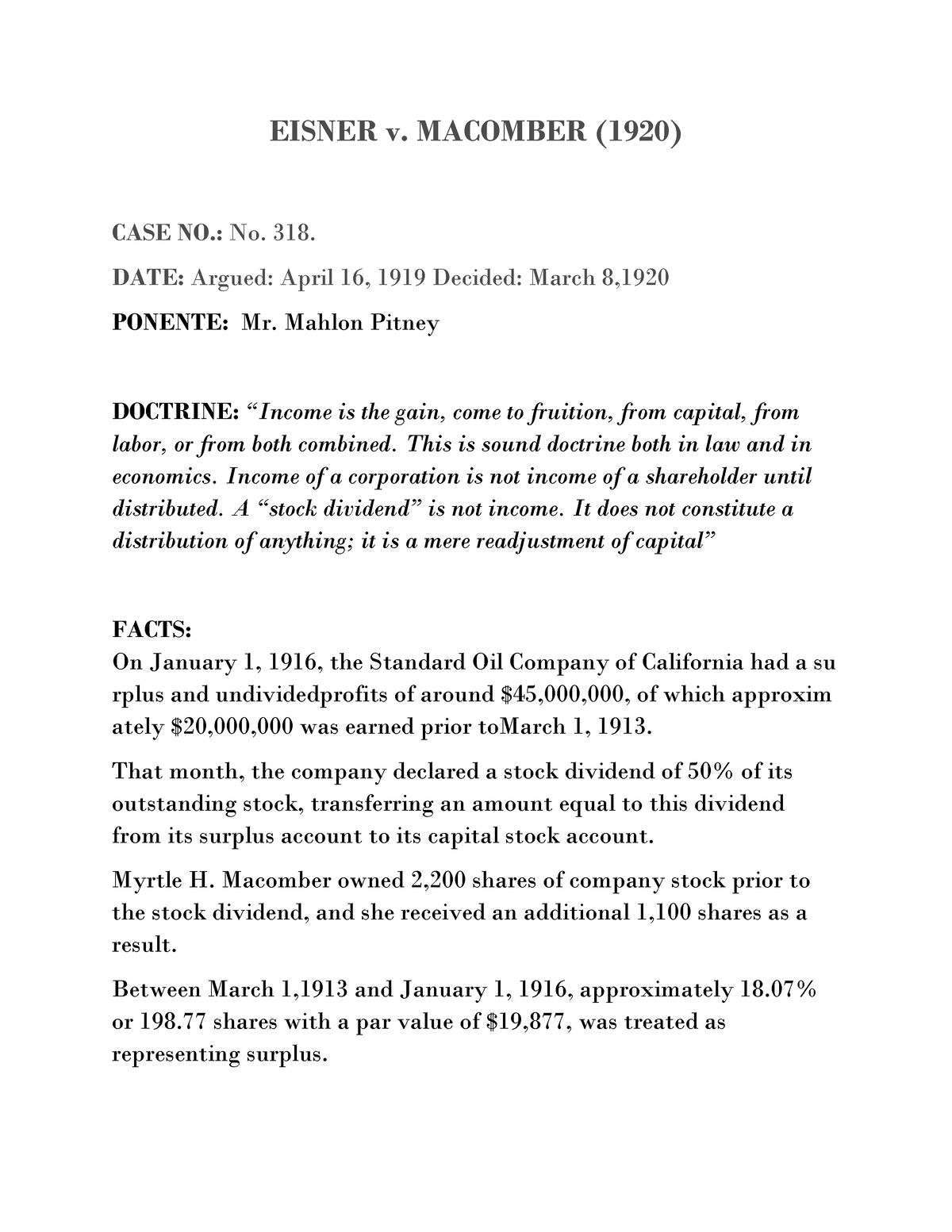

Eisner v. Macomber, 252 U.S. 189 (1920), was a United States Supreme Court case that dealt with the taxation of dividends received by a shareholder. The case involved Frank Eisner, a shareholder in the Macomber company, who received dividends from the company in 1916. Eisner argued that the dividends should not be taxed as income because they were not profits, but rather a return of capital.

The issue in this case was whether dividends received by a shareholder should be treated as income or as a return of capital. The Internal Revenue Service (IRS) argued that dividends were taxable as income because they represented profits earned by the company. However, Eisner argued that dividends were not profits, but rather a return of capital that the shareholder had invested in the company.

The Supreme Court ultimately sided with the IRS, ruling that dividends were taxable as income. In its decision, the Court noted that dividends were a distribution of profits earned by the company and were therefore taxable as income. The Court also pointed out that the purpose of taxation was to raise revenue for the government, and that taxing dividends as income was a way to ensure that all sources of income were subject to taxation.

The decision in Eisner v. Macomber had significant implications for shareholders and the taxation of dividends. It established that dividends were taxable as income, and it clarified the distinction between income and capital. This decision helped to shape the way that dividends are taxed in the United States, and it continues to have an impact on tax law to this day.

Eisner v. Macomber :: 252 U.S. 189 (1920) :: Justia US Supreme Court Center

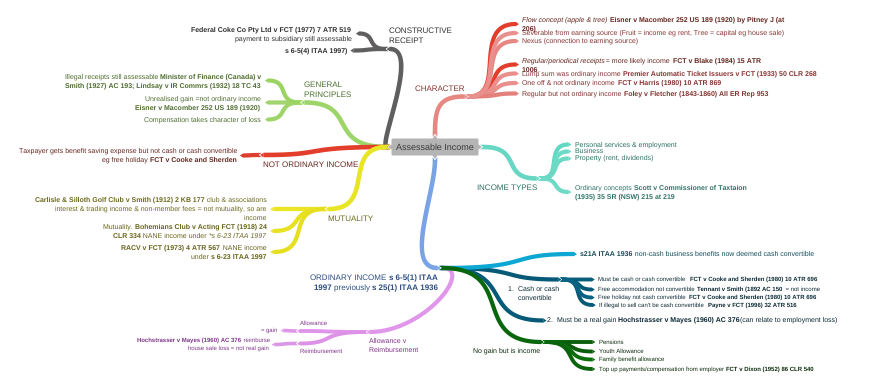

The gains of a business, whether conducted by an individual, by a firm or by a corporation, are ordinarily reinvested in large part. Justice Clifford, in the absence of the debate which about twenty-five years later took place in Pollock v. The ultimate object of corporate business is gain to the stockholders. We adhere to the view then expressed, and might rest the present case there not because that case in terms decided the constitutional question, for it did not, but because the conclusion there reached as to the essential nature of a stock dividend necessarily prevents its being regarded as income in any true sense. Mahon as the rule of administration for the District of Columbia the so-called Massachusetts rule, the opinion being delivered in 1890 by Mr. We will then look at some of the larger tax expenditures in the US and ask how they would fare under constitutional scrutiny part 3. Amendments to such a charter of government ought to be construed in the same spirit and according to the same rules as the original.

Nevertheless, in view of the importance of the matter, and the fact that Congress in the Revenue Act of 1916 declared 39 Stat. The question was, in essence, what shall the intention of the testator be presumed to have been? Or is it as Brandeis thought "more like" the receipt of a cash dividend which is followed by a reinvestment of the cash received in additional shares? Farmers' Loan Trust Co. But is not this equally true of the share of a partner in the year's profits of the firm or, indeed, of the profits of the individual who is engaged in business alone? See Tax Commissioner v. To hold now that earnings both made and paid out after the adoption of the Sixteenth Amendment cannot be taxed as income of the stockholder, if paid in the form of a stock dividend, involves an exceedingly narrow construction of it. The Supreme Judicial Court of Massachusetts has steadfastly adhered, despite ever-renewed protest, to the rule that every stock dividend is, as between life-tenant and remainderman, capital and not income.

TaxConnectionsMoments In Tax History: Income, An Origin Story

January and April; 6 per cent. Financiers, with the aid of lawyers, devised long ago two different methods by which a corporation can, without increasing its indebtedness, keep for corporate purposes accumulated profits, and yet, in effect, distribute these profits among its stockholders. In relevant part, the Revenue Act of 1916 provided that a stock dividend shall be considered income in the amount of its cash value. Other corporations, without this formality, had assumed that the annual accumulating balances carried as undistributed profits were to be treated as capital permanently invested in the business. The law finds no difficulty in disregarding the corporate fiction whenever that is deemed necessary to attain a just result. In each case, he receives a piece of paper which entitles him to certain rights in the undivided property. This court adopted in Gibbons v.

Macomber had been made by the more complicated method pursued by the Standard Oil Company of Kentucky -- that is, issuing rights to take new stock pro rata and paying to each stockholder simultaneously a dividend in cash sufficient in amount to enable him to pay for this pro rata of new stock to be purchased -- the dividend so paid to him would have been taxable as income, whether he retained the cash or whether he returned it to the corporation in payment for his pro rata of new stock. In other words, the substance of the manner of gaining income was the important aspect, not just the form. One method is a simple one. Tax stories: An in-depth look at ten leading federal income tax cases. Mahon, obiter dictum in respect of the matter then before it p.

But we regard the market prices of the securities as an unsafe criterion in an inquiry such as the present, when the question must be not what will the thing sell for, but what is it in truth and in essence. The decision of this Court that earnings made before the adoption of the Sixteenth Amendment, but paid out in cash dividend after its adoption, were taxable as income of the stockholder involved a very liberal construction of the amendment. We refer, of course, to a corporation such as the one in the case at bar, organized for profit, and having a capital stock divided into shares to which a nominal or par value is attributed. If the constitutional power exists to tax corporate earnings when they are passed to the stockholder by means of a cash dividend, no reason is perceived why the same power does not exist to tax the same earnings when they are passed to him, in an equally concrete form, by means of a stock dividend. See Tax Commissioner v. If some other medium is decided upon, it is also wholly a question of financial management whether the distribution shall be, for instance, in bonds, scrip or stock of another corporation or in issues of its own.

There are two insuperable difficulties with this: In the first place, it would depend upon how long he had held the stock whether the stock dividend indicated the extent to which he had been enriched by the operations of the company; unless he had held it throughout such operations the measure would not hold true. The Judicial Committee of the Privy Council sustained the dividend duty upon the ground that, although "in ordinary language the new shares would not be called a dividend, nor would the allotment of them be a distribution of a dividend," yet, within the meaning of the act, such new shares were an "advantage" to the recipients. We ruled at the same term, in Lynch v. Macomber, paid this tax begrudgingly. Chief Justice Marshall in Brown v. Thayer, 7 Harvard Law Review 129, 142. Fourth: The equivalency of all dividends representing profits, whether paid in cash or in stock, is so complete that serious question of the taxability of stock dividends would probably never have been made, if Congress had undertaken to tax only those dividends which represented profits earned during the year in which the dividend was paid or in the year preceding.

After examining dictionaries in common use Bouv. Mahon, it might be desirable for this Court to reconsider the question there decided, as chanrobles. Nothing else answers the description. While several individuals have attempted to use this ruling to protect income tax laws and act as precedence for other arguments, the Supreme Court has appeared to contradict the elements of its ruling in Helvering v. We adhere to the view then expressed, and might rest the present case there; not because that case in terms decided the constitutional question, for it did not; but because the conclusion there reached as to the essential nature of a stock dividend necessarily prevents its being regarded as income in any true sense. How these two methods have been employed may be illustrated by the action in this respect as reported in Moody's Manual, 1918 Industrial, and the Commercial and Financial Chronicle of some of the Standard Oil companies since the disintegration pursuant to the decision of this Court in 1911.

This is sound doctrine both in law and in economics. It is a statement of general principles, and not a specification of details. His gain comes, not from the declaration of a dividend of any kind, but from what his capital has earned. Business men, dealing with the problem practically, fix necessarily periods and rules for determining whether there have been net profits — that is income or gains. Clearly segregation of assets in a physical sense is not an essential of income.

Hayden, 102 Massachusetts, 542. This gain always and necessarily first appears in the shape of undivided profits which are held in trust for them. If a stock dividend is not considered income, it can not be subject to income tax under the 16th Amendment. Suppose that a corporation having power to buy and sell its own stock, purchases, in the interval between its regular dividend dates, with monies derived from current profits, some of its own common stock as a temporary investment, intending at the time of purchase to sell it before the next dividend date and to use the proceeds in paying dividends, but later, deeming it inadvisable either to sell this stock or to raise by borrowing the money necessary to pay the regular dividend in cash, declares a dividend payable in this stock: — Can anyone doubt that in such a case the dividend in common stock would be income of the stockholder and constitutionally taxable as such? In dismissing the appeal these words of the Chief Justice of the Supreme Court of Western Australia were quoted p. But if a shareholder sells dividend stock, he necessarily disposes of a part of his capital interest, just as if he should sell a part of his old stock, either before or after the dividend. What was said by this Court upon the latter question is equally true for the former.