How to calculate predetermined manufacturing overhead rate. How To Calculate Predetermined Overhead Rate (With Examples) 2022-12-17

How to calculate predetermined manufacturing overhead rate Rating:

9,4/10

1397

reviews

Calculating a predetermined manufacturing overhead rate is an important part of cost accounting in a manufacturing business. It involves determining the expected overhead costs for a given period of time, and dividing these costs by the expected level of production or activity during that period. This calculation is used to assign overhead costs to the products or services being produced, allowing the business to accurately track and understand the costs associated with each unit of production.

There are several steps involved in calculating a predetermined manufacturing overhead rate:

Identify the overhead costs: The first step is to identify all of the overhead costs that will be included in the calculation. These costs may include indirect materials, indirect labor, utilities, rent, and other indirect costs that are not directly associated with a specific product or service.

Determine the allocation base: The allocation base is the measure of activity or production that will be used to divide the overhead costs. This could be the number of units produced, the number of direct labor hours, or some other measure that is relevant to the business.

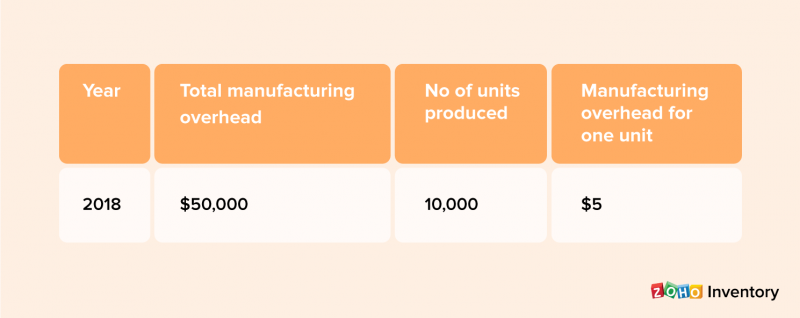

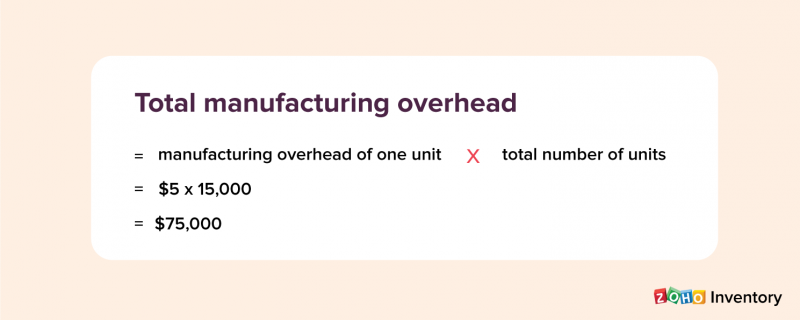

Calculate the overhead rate: Once the overhead costs and allocation base have been identified, the predetermined manufacturing overhead rate can be calculated by dividing the total overhead costs by the allocation base. For example, if the total overhead costs are $100,000 and the allocation base is 10,000 units, the predetermined manufacturing overhead rate would be $10 per unit.

Apply the overhead rate to production: Once the predetermined manufacturing overhead rate has been calculated, it can be used to assign overhead costs to the products or services being produced. This is typically done by multiplying the overhead rate by the number of units produced or the number of direct labor hours used.

Monitor and adjust the overhead rate: It is important to regularly review and adjust the predetermined manufacturing overhead rate to ensure that it accurately reflects the actual overhead costs of the business. This may involve adjusting the allocation base or the overhead costs themselves, as necessary.

By following these steps, a manufacturing business can accurately calculate and apply a predetermined manufacturing overhead rate, which allows it to track and understand the costs associated with its products or services. This information is critical for making informed business decisions and improving profitability.

How to Calculate Manufacturing Overhead Costs

This estimated overhead rate will allow a company to determine a cost for the product without having to wait, possibly several months, until all of the actual overhead costs are determined, and to help with issues such as seasonal production or variable overhead costs, such as utilities. Manufacturing overhead, also known as production overhead or factory overhead, refers to all the indirect costs a company incurs in the manufacturing process. What are engine hours? What are some examples of overhead costs? Do engine hours include idle hours? Conversely, a high manufacturing overhead rate indicates a lagging and inefficient production process. The business owner can then add the predetermined overhead costs to the cost of goods sold to arrive at a final price for the candles. Predetermined overhead rate is calculated by dividing the manufacturing overhead cost by the activity driver. These are: Fixed manufacturing overhead Fixed overhead are costs that remain unchanged irrespective of the company's quantity of goods. Step 3: Next, decide on the allocation base for the period, which can be direct labor cost, direct labor hours, machine hours or prime cost.

How To Calculate Predetermined Overhead Rate (With Examples)

Many or all of the products here are from our partners that pay us a commission. Often, the actual overhead costs experienced in the coming period are higher or lower than those budgeted when the estimated overhead rate or rates were determined. Using a predetermined rate, companies can assign overhead costs to production when they assign direct materials and direct labor costs. This allocation can come in the form of the traditional overhead allocation method or activity-based costing. Similarly, businesses and other organizations must create an allocation system for assigning limited resources, such as overhead. It might also include supplies employees need to keep the factory running smoothly.

The total manufacturing overhead cost will be the variable overhead plus fixed overhead. Apply Overhead Multiply the overhead allocation rate by the actual activity level to get the applied overhead for your cost object. What is fixed manufacturing overhead? However, only those staff members are taken into account when calculating overhead, such as maintenance staff, factory supervisors, and cleaning teams, whose jobs are directly related to manufacturing. For example, a company pays more for utilities such as electricity, fuel and water if it produces 100,000 units of products than when it makes 10,000 units. Job order costing traces the costs directly to the product, and process costing traces the costs to the manufacturing department. Are engine hours the same as clock hours? Example This example helps to illustrate the predetermined overhead rate calculation. Machine hour rate is the cost of running a machine per hour.

How to Calculate Predetermined Overhead Rate in 4 Steps

Also, if the rates determined are nowhere close to being accurate, the decisions based on those rates will be inaccurate, too. A gasoline engine can last anywhere from 1,500 to 8,000 hours on average whereas a diesel engine can lasting anywhere from 8,000 to 9,000 hours on average. How many hours is a semi engine? Manufacturing companies calculate this overhead cost for every product unit to arrive at a feasible unit price. Musicality uses this information to determine the cost of each product. The best way to predict your overhead costs is to track these costs on a monthly basis. How to calculate predetermined overhead rate.

Larger organizations employ different allocation bases for determining the predetermined overhead rate in each production department. Those advantages come at a cost, both in resources and time, since additional information needs to be collected and analyzed. Manufacturing overhead covers all the indirect costs necessary to keep operations running. It can also help them know when to review their spending more closely, so they can protect the company's profit margins. Can you absorb all of the fixed manufacturing overhead? What is the meaning of predetermined overhead rate? How do you calculate fixed manufacturing overhead? Manufacturing companies use these utilities for various purposes, such as power generations, machine operation, facility lighting, temperature regulation and other functions.

How to Calculate Manufacturing Overhead (With Examples)

Examples can include machine maintenance, utility expenses, factory supplies, and equipment depreciation. If you are in charge of a factory, you must make an educated guess as to how long each machine will operate each day. To estimate the level of activity, sales and production budget can be used. Companies typically base their predetermined overhead rateson the estimated, or budgeted, amount of allocation base for the upcoming period. After the activity level for the selected base and the factory overhead have been estimated, the overhead rates can be computed. How do you calculate the allocation rate Poh? Manufacturing units need factory supplies, electricity and power to sustain their operations. How Do You Calculate Allocated Manufacturing Overhead? However, in recent years the manufacturing operations have started to use machine hours more predominantly as the allocation base.

If you want to learn more about running and scaling a successful eCommerce business, subscribe to our blog. This can result in abnormal Unexpected expenses can be a result of a big difference between actual and estimated overheads. Solution: From the above list, salaries of floor managers, factory rent, depreciation and property tax form part of manufacturing overhead. But determining the exact overhead costs is not easy, as the cost of electricity needed to dry, crush, and roast the nuts changes depending on the moisture content of the nuts upon arrival. Written by Updated on September 17, 2021 Predetermined Overhead Rate: Definition A predetermined overhead rate is an allocation rate given for indirect manufacturing It is used to estimate future manufacturing costs.

What is the machine hour rate? Its production department comes up with the details of how much the overheads will be and what other costs will be incurred. The common allocation bases are direct labor costs, direct labor hours, machine hours and direct materials. This information can help you make decisions about where to cut costs or how to allocate your resources more efficiently. This can help you assign costs accurately and predict expenses successfully. Calculate the Total Manufacturing Overhead To calculate the manufacturing overhead, identify the manufacturing overhead costs that help production run as smoothly as possible.

6.1 Calculate Predetermined Overhead and Total Cost under the Traditional Allocation Method

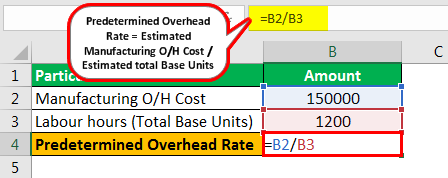

CFO needs you as the cost accounting to calculate the overhead rate for this coming year. Fixed costs are those that remain the same even when production or sales volume changes. A predetermined overhead rate is calculated at the start of the accounting period by dividing the estimated manufacturing overhead by the estimated activity base. Registration with the SEC does not imply a certain level of skill or training. This chapter will explain the transition to ABC and provide a foundation in its mechanics. An industrial producer of plastic storage containers may choose total hours of active machine operation as the driver. You need more than labor and raw materials to manufacture products.