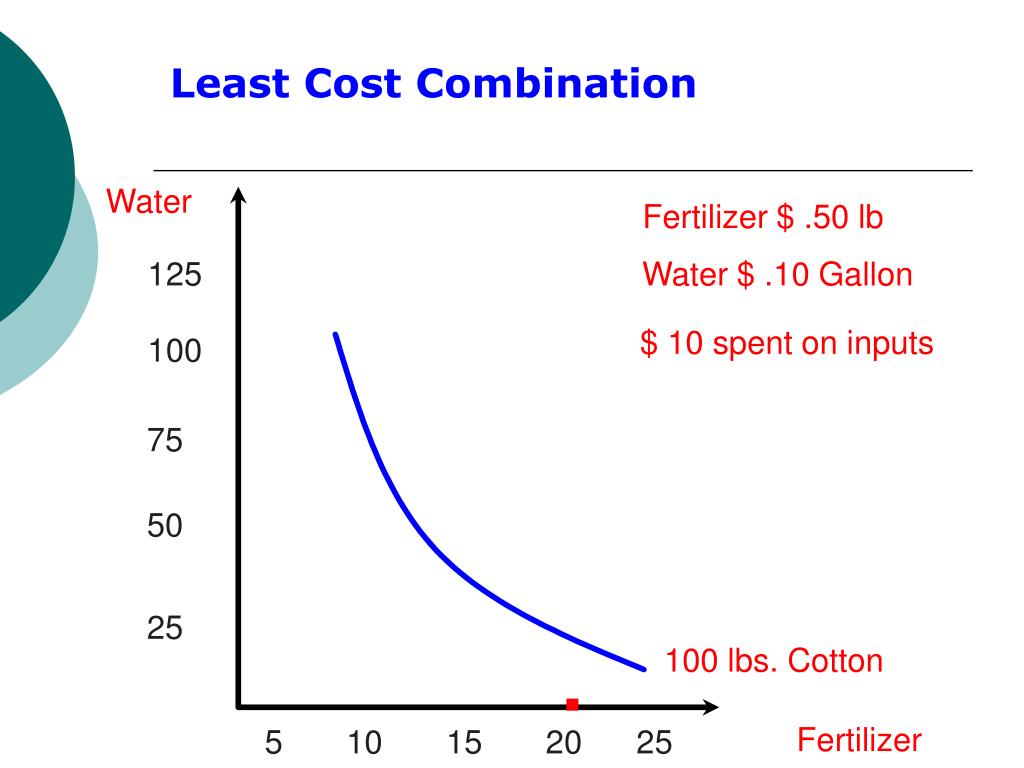

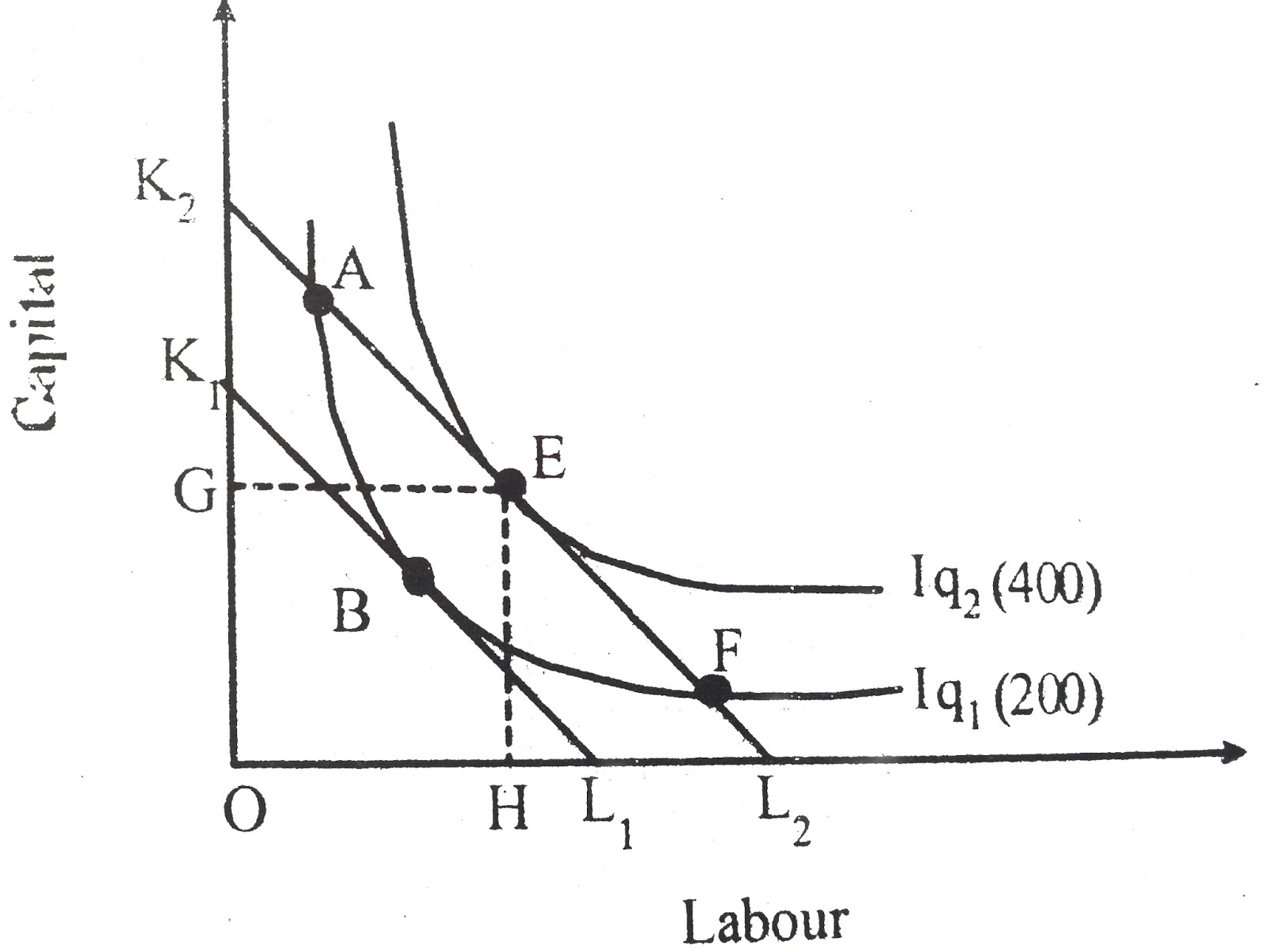

The least cost combination of inputs refers to the mix of inputs (such as labor, capital, raw materials, etc.) that a business or organization uses to produce a particular good or service in the most cost-effective manner. Determining the least cost combination of inputs is an important aspect of cost-benefit analysis, as it allows businesses to minimize their production costs and increase their profitability.

There are several factors that can affect the least cost combination of inputs. These include the availability and cost of different inputs, the technology and production processes used, and the market demand for the final product. For example, if labor costs are high but capital costs are low, a business may choose to use more capital-intensive production methods in order to reduce labor costs and increase efficiency. On the other hand, if raw materials are cheap and abundant, a business may choose to use more of these inputs in order to lower production costs.

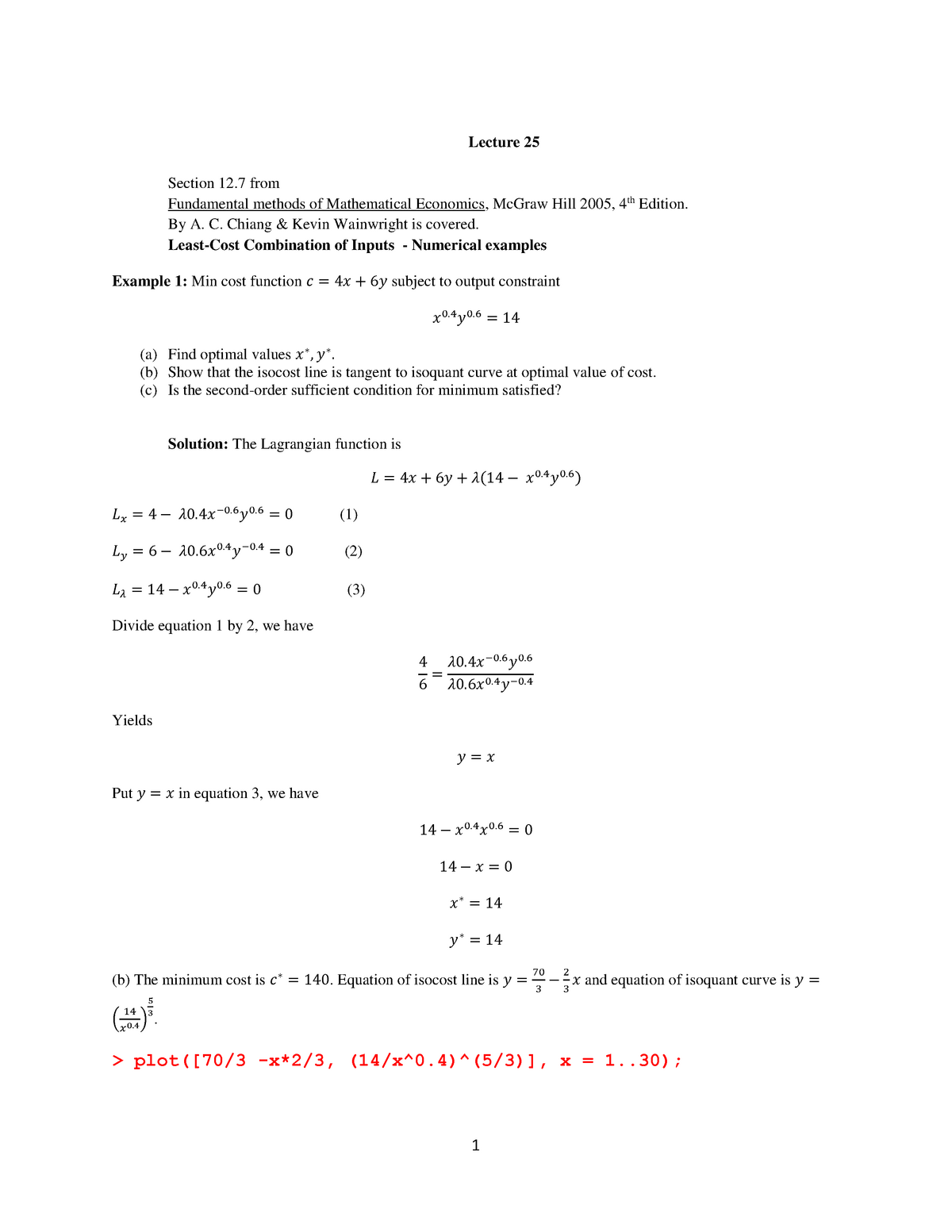

One way to determine the least cost combination of inputs is through the use of production functions, which describe the relationship between inputs and output. By analyzing the production function and calculating the marginal product of each input, businesses can identify the point at which the marginal cost of an input equals its marginal revenue, known as the marginal cost-marginal revenue rule. This rule allows businesses to determine the optimal mix of inputs that will maximize their profits.

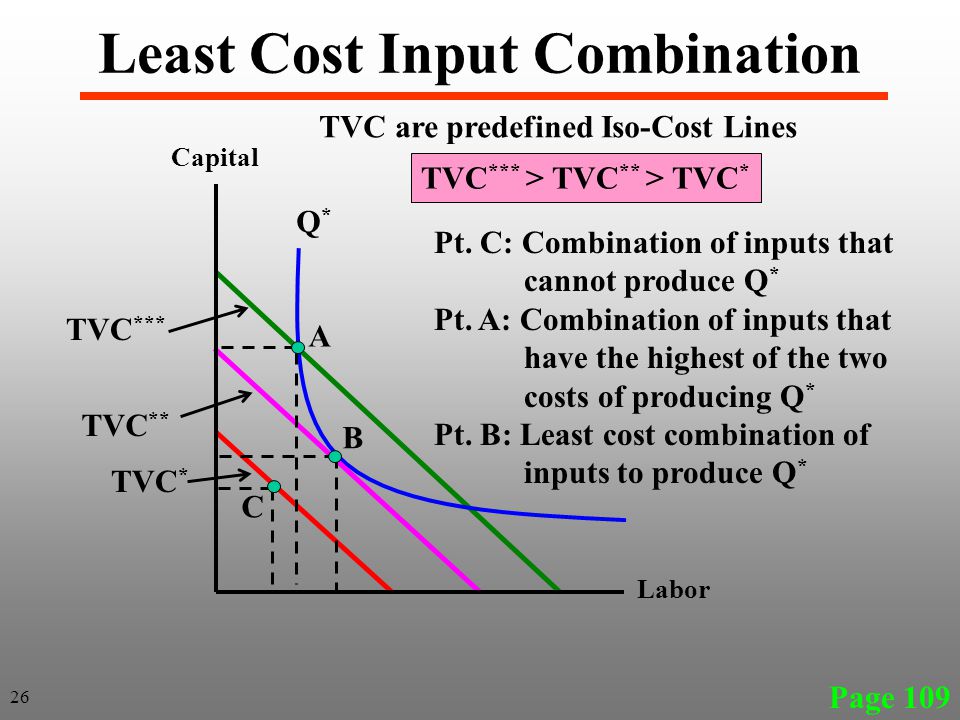

Another approach is to use cost-minimization analysis, which involves comparing the costs of producing a good or service using different combinations of inputs. This allows businesses to identify the combination of inputs that will result in the lowest production costs, given the prices of the inputs and the level of output desired.

In addition to minimizing production costs, businesses may also consider other factors when determining the least cost combination of inputs. For example, they may consider the environmental impact of different inputs or the potential for future cost changes.

Overall, the least cost combination of inputs is an important concept for businesses and organizations looking to increase efficiency and profitability. By carefully analyzing the costs and benefits of different input combinations, businesses can make informed decisions about how to produce goods and services in the most cost-effective manner.