Marginal cost of output. Marginal Cost of Production 2022-12-26

Marginal cost of output Rating:

7,2/10

392

reviews

The marginal cost of output is the cost of producing an additional unit of a good or service. It represents the increase in total cost that a firm incurs when it produces one more unit of output. In other words, it is the cost of the additional inputs required to produce one more unit of output.

The marginal cost of output is an important concept in economics because it helps firms to make production decisions. By understanding the marginal cost of output, firms can determine the optimal level of production, at which the marginal cost is equal to the marginal revenue. This is known as the point of profit maximization.

There are several factors that can affect the marginal cost of output. One of the most important is the degree of variable inputs used in the production process. For example, if a firm uses more labor or raw materials in the production of an additional unit of output, the marginal cost will be higher. The state of technology also plays a role in the marginal cost of output, as advances in technology can reduce the cost of production.

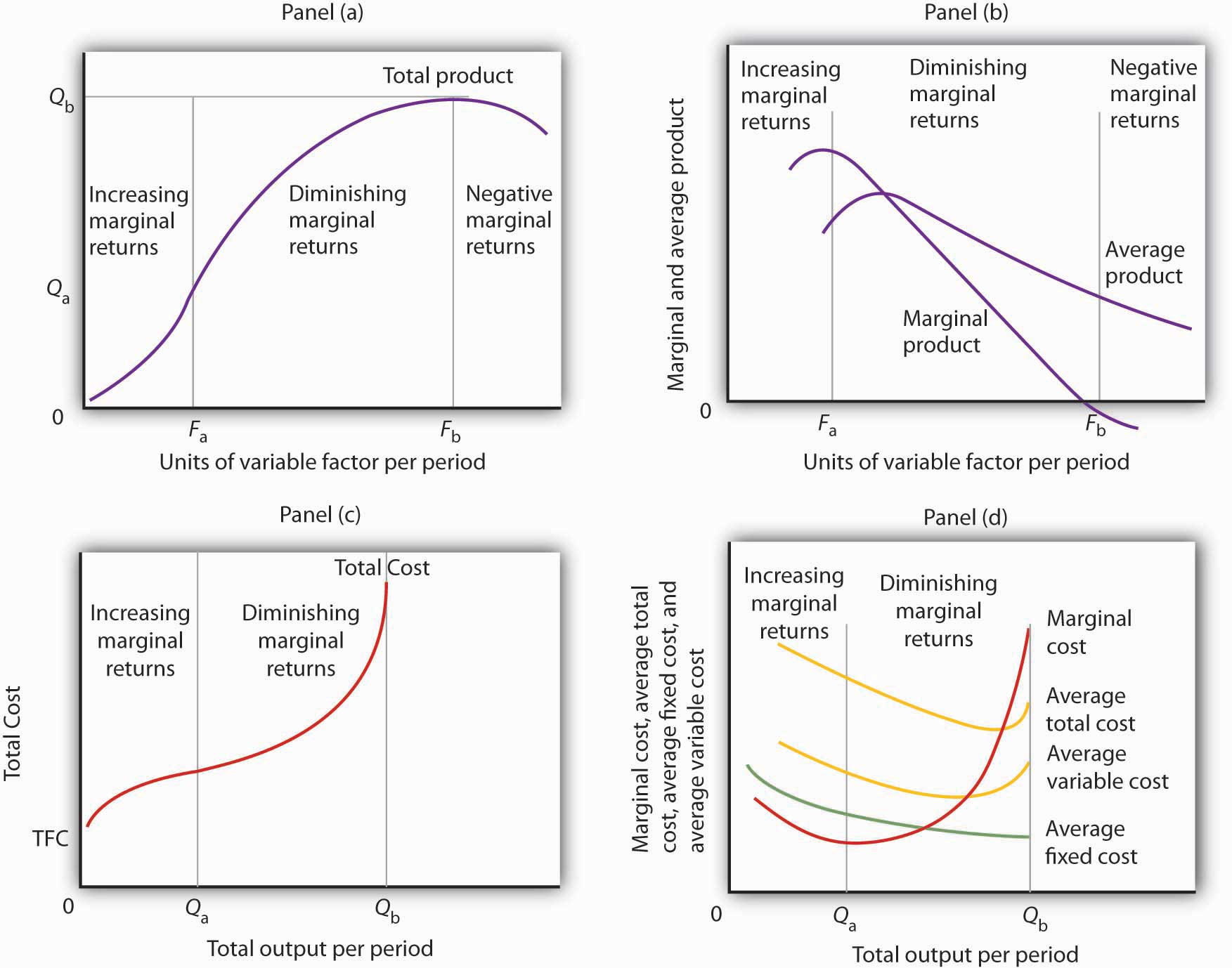

In the short run, the marginal cost of output can also be affected by fixed costs. Fixed costs are costs that do not change with the level of output, such as rent or property taxes. In the short run, when a firm is operating at a fixed level of production, the marginal cost of output will be equal to the variable cost per unit of output, plus the fixed cost per unit of output. In the long run, when a firm has the ability to adjust all of its inputs, the marginal cost of output will be equal to the variable cost per unit of output.

Understanding the marginal cost of output is important for firms because it helps them to make informed production decisions. By understanding the marginal cost of output, firms can determine the optimal level of production, at which they will maximize profits. It is also important for policy makers, as it can help them to understand the potential impacts of changes in the cost of inputs or technological advances on the cost of production and the competitiveness of firms in an industry.

Marginal Cost of Production

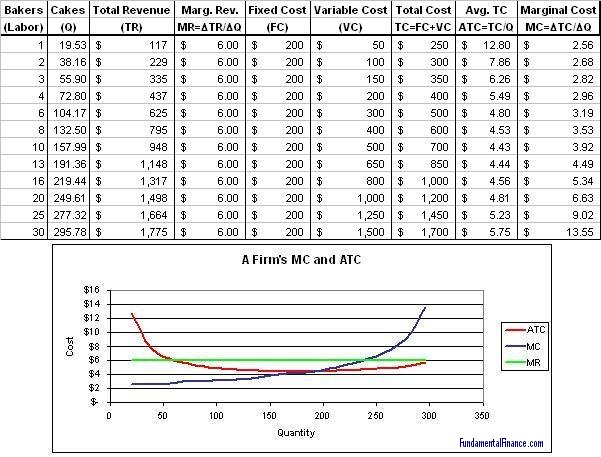

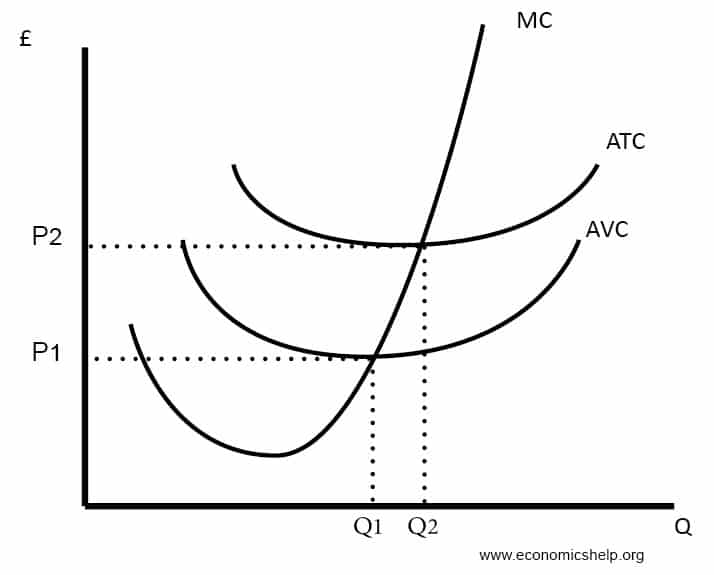

When marginal cost is less than average cost, average cost falls and when marginal cost is greater than average cost, average cost rises. Long-run marginal cost of production The long-run marginal cost of production is the increased cost incurred during production when every input is variable. Typically, costs will increase as more raw materials, machinery, and labor are required to produce more. Therefore, the production of additional units becomes cheaper, hence maximizing their profits while minimizing the marginal cost of production. The cost of producing a unit can vary according to the volume of the goods produced. It also enables companies to gauge the effects of changes in production.

How to Find Marginal Cost: 11 Steps (with Pictures)

Consider the warehouse for a manufacturer of landscaping equipment. In economics, the profit metric equals revenues subtracted by costs. In economics, the profit metric equals revenues subtracted by costs. Last Update: October 15, 2022 This is a question our experts keep getting from time to time. When marginal costs are plotted on a graph, you should be able to see a U-shaped curve where costs begin high but they shift and go down as production increases.

Marginal cost also takes into consideration the cost of opportunity, which is the value of the next best alternative foregone when making a decision. Alicia Tuovila is a certified public accountant with 7+ years of experience in financial accounting, with expertise in budget preparation, month and year-end closing, financial statement preparation and review, and financial analysis. For example, overproduction beyond a specific level may require overtime pay for workers and increased machinery maintenance costs. A rise or decline in the output volume production eventually is reflected in the overall cost of production and as such it is important to know the change. Therefore, it needs to recover all production costs and operate profitably.

Companies can better control their production costs by focusing on variable costs and passing on those savings to their customers without compromising quality. However, the market has a higher demand for mattresses the next year, which requires the production of more units. This will likely occur when manufacturing needs to increase or decrease output volume. The marginal cost of production may be defined as the costs incurred for each extra output produced. For example, if 3,000 pairs of shoes were made in an initial production run but 10,000 more need to be made, you could calculate the change in quantity by deducting the number of shoes made in the first run from the volume of output in the second. Unlike the short-run cost curve, the long-run marginal cost curve is flat.

Does marginal cost increase as output increases? Explained by FAQ Blog

Leather and plastic are variable costs as the costs increases as the quantity of shoes produced increases. Fixed costs Fixed costs remain constant and do not change with a decrease or increase in production output. The cost of producing the next unit of output is then reduced. You can calculate the total fixed cost by subtracting your total variable costs from your total production cost. Here we discuss its uses along with practical examples. Now, we have got a complete detailed explanation and answer for everyone, who is interested! Difference Between Variable Cost vs. In economics, the marginal cost is the change in total production cost that comes from making or producing one additional unit.

Marginal cost is the incremental change in total cost resulting from producing one more unit of a good or service. You can calculate them using simple arithmetic operations. Say, with the current capacity; the company can still increase its output to 24 units. But, if they also produce a few more sandwiches, they will need to increase their kitchen space, staff, and ingredients. The lower the total cost, the more profit a firm can generate.

Marginal cost and revenue: Formulas, definitions, and how

However, companies working with diseconomies of scale experience higher production costs per unit as more outputs are produced. Although the total cost is comprised of fixed cost and variable costs, the variation in total cost due to a change in the quantity of production is primarily because of variable cost which includes labor and material cost. Average cost is the total cost divided by the total number of units produced. What happens when marginal product decreases? A company managed to increase its production to 20 units. The marginal cost of production is used to measure the change in the cost of a product resulting from the production of an extra unit of output.

The capacity adjustment is the additional amount of physical or labor capital that a firm would need in the long run to produce an additional unit of the finished product. Knowing marginal cost enables the organization to determine and come up with an optimal revenue margin for sustaining sales and increasing profits. Why is Marginal Cost Important? Fixed Cost A thorough understanding of the difference between fixed and variable costs is crucial for rational decision-making. When you consider all of these costs, you will realize that they contribute to the overall cost structure of your business. When marginal cost exceeds marginal revenue, it is no longer financially profitable for a company to make that additional unit as the cost for that single quantity exceeds the revenue it will collect from it. Importance of the Marginal Cost of Production After determining the relationship between the marginal cost of production and marginal revenue , it is easier for a company to plan production levels and put in place per unit pricing strategies.