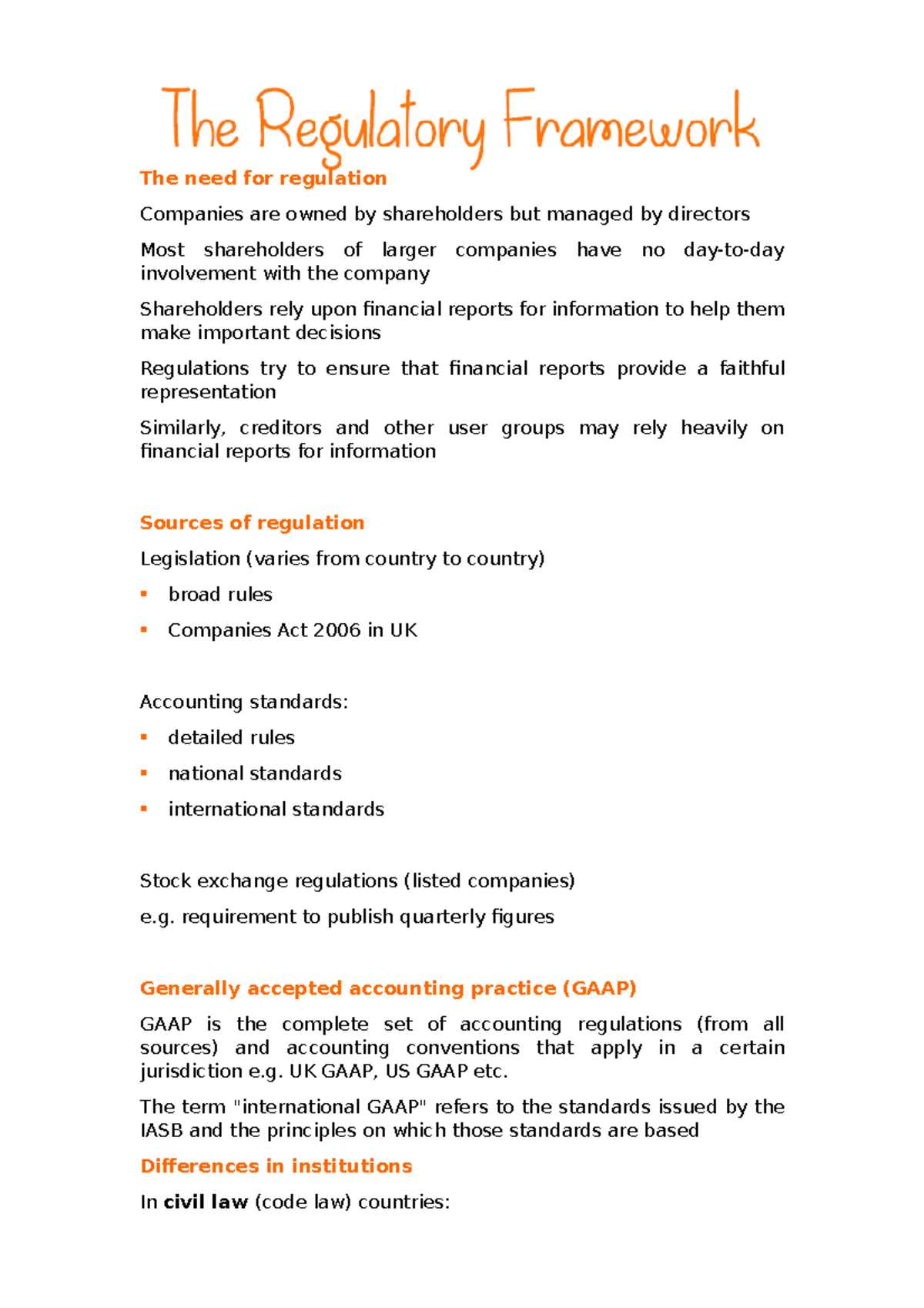

Sources of gaap. Generally Accepted Accounting Principles (United States) 2022-12-14

Sources of gaap Rating:

9,8/10

764

reviews

Law is a vast and multifaceted field, with a wide range of topics that could be explored in a dissertation. As a law student, you have the opportunity to delve into a subject that interests you and make a meaningful contribution to the legal discourse. Here are a few ideas for dissertation topics that might be of interest to law students:

The impact of international law on domestic legal systems: This topic could explore how international law is incorporated into domestic legal systems, and the ways in which it impacts the interpretation and application of domestic laws.

The role of human rights in criminal justice: This topic could examine the intersection of human rights and criminal justice, and explore how human rights are protected and promoted within the criminal justice system.

The use of alternative dispute resolution in commercial law: This topic could explore the use of alternative dispute resolution methods, such as mediation and arbitration, in commercial law, and consider the benefits and drawbacks of these approaches compared to traditional litigation.

The legal regulation of artificial intelligence: As AI becomes increasingly prevalent in our society, it is important to consider the legal implications of its use. This topic could explore the ways in which AI is regulated by law, and consider the challenges and opportunities presented by this rapidly evolving technology.

The role of law in addressing environmental challenges: This topic could explore the ways in which law is used to address environmental issues, such as climate change, pollution, and natural resource management.

These are just a few examples of the many potential dissertation topics that might be of interest to law students. Ultimately, the best topic for your dissertation will depend on your interests and goals, as well as the current state of the field and the needs of your academic community.

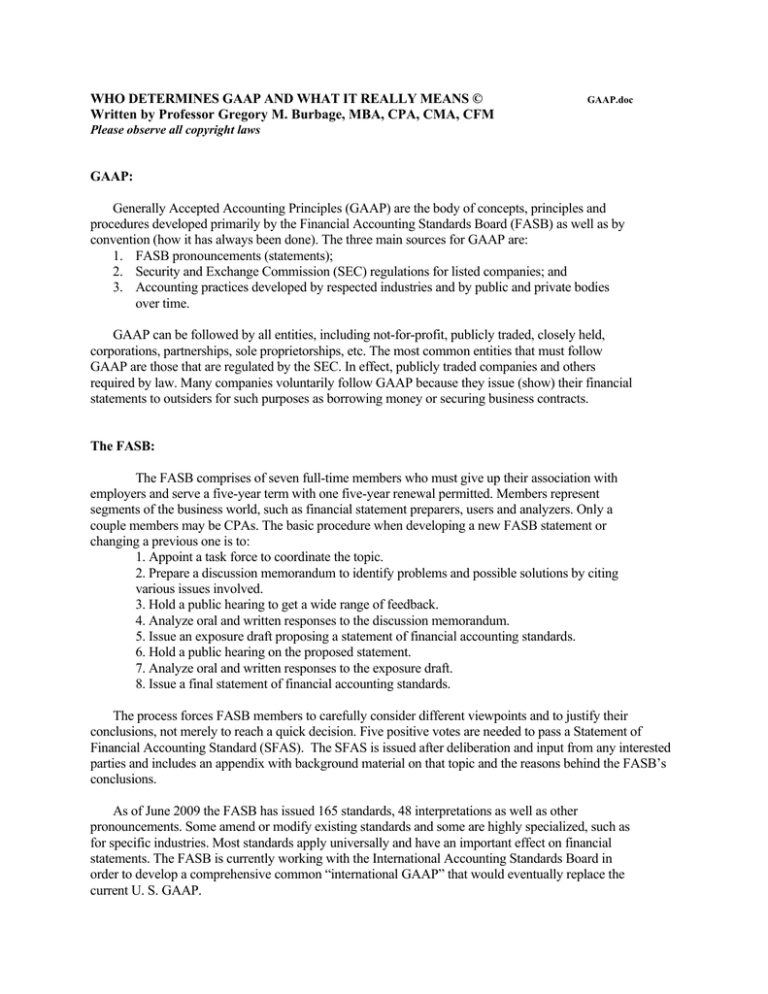

Generally Accepted Accounting Principles (United States)

The consistency of presentation of financial reports that results from GAAP makes it easy for investors and other interested parties such as a board of directors to more easily comprehend financial statements and compare the financial statements of one company with those of another company. The Wall Street Journal. Needed Complete Accounting Solution contact My Name is Nadeem Shaikh the founder of nadeemacademy. When auditors do not mention consistency in the auditors' report, a reader of the financial statements may infer A. Auditing: An Integrated Approach. Generally accepted accounting principles, or GAAP, are standards that encompass the details, complexities, and legalities of business and corporate accounting. Nothing about application of accounting principles within the period.

Governmental Accounting, Auditing, and Financial Reporting. The SEC has the authority to both set and enforce accounting standards. Principle of Consistency Accountants commit to applying the same standards throughout the reporting process, from one period to the next, to ensure financial comparability between periods. Consistent with all sources of taxable income, and to the extent necessary under the relevant tax law, the character of the uncertain tax position should be considered. IFRS concentrates more on the general principles of GAAP which results in it easier to understand the IFRS corpus of research smaller, simpler, and easier to understand as compared to GAAP. The Codification is effective for interim and annual periods ending after September 15, 2009. An item is considered significant when it would affect the decision of a reasonable individual.

Rule of Consistency: GAAP certified accountants adhere to the established guidelines and rules and. The Financial Accounting Standards Board FASB , an independent nonprofit organization, is responsible for establishing these accounting and financial reporting standards. Topic 2: Describe effective accounting information using the qualities of accounting information from your readings this week. No one should act upon such information without Premium Balance sheet Financial statements Generally Accepted Accounting Principles Gaap What is the prudence concept in accounting? In 1984, the FASB created the Emerging Issues Task Force EITF. The US GAAP is a comprehensive set of accounting practices that were developed jointly by the Financial Accounting Standards Board FASB and the Governmental Accounting Standards Board GASB , so they are applied to governmental and non-profit accounting as well.

The uniformity of GAAP compliance also permits companies to better evaluate the strategic business alternatives. The Principle of Prudence : states that speculation should affect the reporting of financial information. Auditors are required to ensure that their financial statements be prepared in compliance with GAAP Soffer, 1993. These organizations are rooted in historical regulations regarding financial reporting that the federal government enacted in 1929 following the stock market crash that led to the Great Depression. GAAP seeks to improve the consistency, clarity, and comparability of the reporting and reporting of information about financials.

This report is about the evaluation of the convergence project to form a global standardized financial statement. The international alternative to GAAP is the International Financial Reporting Standards IFRS , set by the The IASB and the FASB have been working on the convergence of Due to the progress achieved in this partnership, the SEC, in 2007, removed the requirement for non-U. Identify source hierarchy and explain why the hierarchy is important. Several sources of GAAP consulted by auditors are in conflict as to the application of an accounting principle. GAAP pronouncements into roughly 90 accounting topics. Revenue and expense should be kept separate from personal expenses.

FASB Statements of Financial Accounting Concepts D. What are your major sources of stress? Both GAAP and IFRS require investments to be segregated into discrete categories based on asset type. While the two systems have different principles, rules, and guidelines, IFRS and GAAP have been working towards merging the two systems. These are often referred to as "Rule 203 Pronouncements" because it was under this rule that Council was given permission to designate specific bodies to establish accounting principles "ET Section 203", 1993. Should there be a conflict between practices from sources found in more than one category, than the treatment specified in the higher category is expected to be followed. Principiality of Periodicity: The reporting of income is divided into traditional accounting dates, such as fiscal quarters or fiscal year.

Several sources of GAAP consulted by auditors are in conflict as to the

That no material departure from GAAP has been detected C. They are a combination of authoritative standards set by policy boards and are simply the commonly accepted way of recording and reporting accounting information. GAAP and Private Companies Although they are not required to follow GAAP, private companies may choose to do so, especially if they wish to obtain loans or other financing, and if they have long-term plans to seek funding from private equity firms and institutionalize the company to be ready for public listing. Companies are still allowed to present certain figures without abiding by GAAP guidelines, provided that they clearly identify those figures as not conforming to GAAP. GAAP also seeks to make non-profit and governmental entities more accountable by requiring them to clearly and honestly report their finances.

What are the basic Principles of Accounting? Some companies may report both GAAP and non-GAAP measures when reporting their financial results. GAAP includes three elements that prevent misleading practices in accounting and practice of financial report. For this reason, the AICPA, in their Statement of Auditing Standards No. As they are not part of the Codification, they are not authoritative GAAP. GAAP is more rules-based than IFRS. The principle of non-compensation : is that all aspects the performance of an organization, either positive or not, is documented without the possibility or compensation from debt.

However, this problem-by-problem approach failed to develop the much needed structured body of accounting principles. In the end, there will be minimal distinctions in the reported results of a company if it chooses to switch between both. GAAP is a set of procedures and guidelines used by companies to prepare their financial statements and other accounting disclosures. They are related to computer software developed for external use is capitalized once technological feasibility is established in accordance with specific critical area. GAAP convergence with IFRS There are various working groups which are slowly diminishing the differences between GAAP and IFRS accounting systems. AICPA Technical Practice Aids Difficulty: Hard Source: AICPA 29.

Not what you're looking for? Presentation: What line items or Subtotals and totals should be shown within the statements of financials and what ways can they be combined in the financial statements Information on disclosure: what specific information is crucial to the readers of those financial documents. What is a GAAP and why is it important? I am a Qualified Chartered Accountant, B. During 1939 to 1959 CAP issued 51 Accounting Research Bulletins that dealt with a variety of timely accounting problems. In other words, it should not compensate offset a debt with an asset. It also includes relevant To prepare users for the change, the AICPA While the Codification does not change GAAP, it introduces a new structure—one that is organized in an easily accessible, user-friendly online research system.