Cash flow estimation and risk analysis. Chapter 12 Cash Flow Estimation and Risk 2022-12-28

Cash flow estimation and risk analysis Rating:

5,3/10

661

reviews

Cash flow estimation and risk analysis are important tools for businesses, investors, and financial analysts. They help to understand the financial health of a company and identify potential problems or opportunities. In this essay, we will explore the importance of cash flow estimation and risk analysis, how they are used, and some of the challenges involved in these processes.

Cash flow estimation is the process of predicting the amount of cash that a business will generate and receive over a specific period of time. It is a key component of financial planning and decision-making, as it helps to determine the feasibility of investments, loans, and other financial commitments. Cash flow can be estimated using various methods, including the direct method, which involves calculating the cash inflows and outflows based on actual transactions, and the indirect method, which involves starting with net income and adjusting for changes in non-cash items such as depreciation.

Risk analysis, on the other hand, is the process of evaluating the potential risks that a business or investment may face. It is an important step in the decision-making process, as it helps to identify and quantify the potential consequences of different courses of action. Risk analysis can be done qualitatively, by considering the likelihood and impact of different risks, or quantitatively, by using mathematical models to calculate the probability and potential consequences of different risks.

There are several challenges involved in cash flow estimation and risk analysis. One challenge is the accuracy of the predictions. Cash flow estimates are based on assumptions about future events, and these assumptions may not always be accurate. Similarly, risk analysis involves predicting the likelihood of different risks occurring, and this can be difficult due to the inherent uncertainty of the future. Another challenge is the complexity of the processes involved. Cash flow estimation and risk analysis require a thorough understanding of financial principles and the ability to analyze complex data. Finally, there is the issue of bias, which can arise when estimators and analysts have conflicting interests or preconceived notions about the outcomes they want to see.

In conclusion, cash flow estimation and risk analysis are essential tools for businesses and investors. They help to understand the financial health of a company and identify potential risks and opportunities. While there are challenges involved in these processes, the benefits of accurate and informed decision-making make them worth the effort.

CASH FLOW ESTIMATION AND RISK ANALYSIS Flashcards

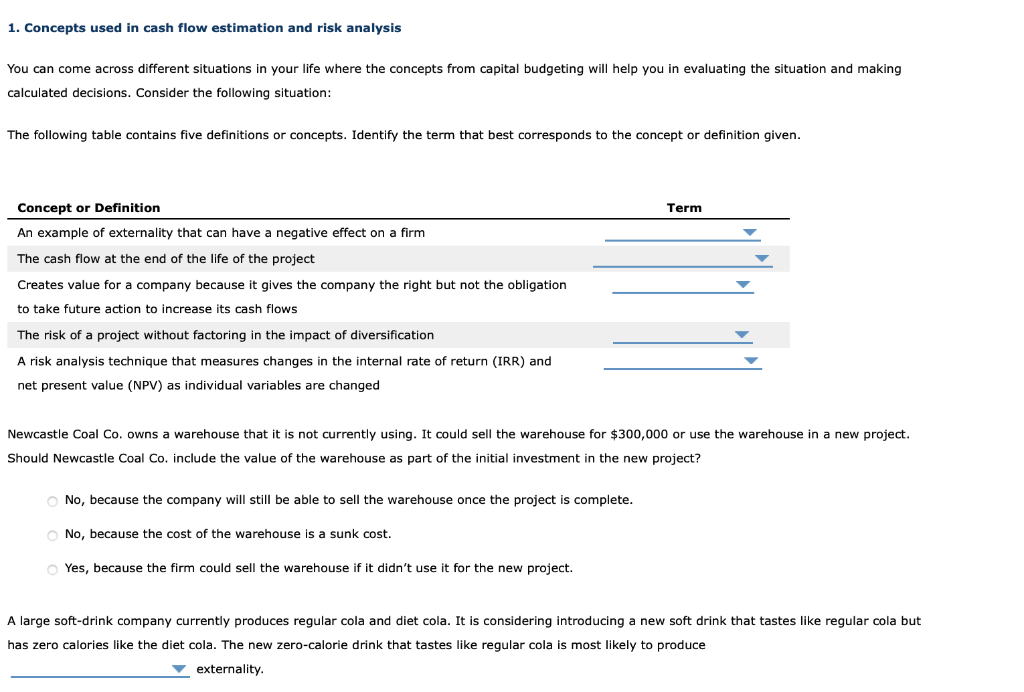

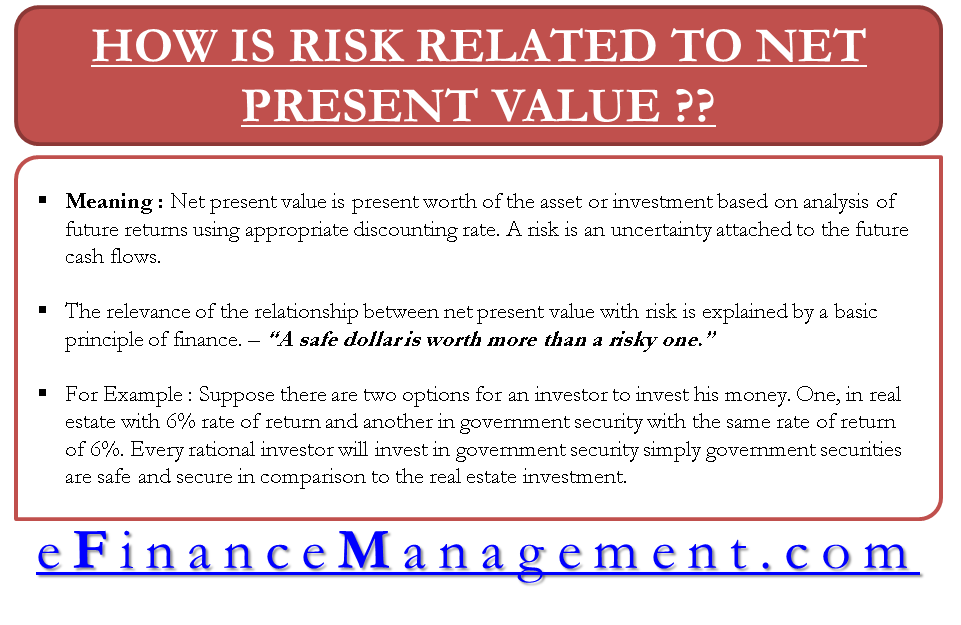

PBP is the duration it takes to recover the initial capital of an investment. The equipment has a 3-year tax life and would be fully depreciated by the straight-line method over 3 years, but it would have a positive pre-tax salvage value at the end of Year 3, when the project would be closed down. Should the project be accepted? In theory, this type of risk should be of little or no concern. NPV expresses the wealth generation impact of an investment in dollar terms. DAYS ON CHAPTER: 4 OF 58 DAYS 50 - minute periods 304 Lecture Suggestions Chapter 12 : Cash Flow Estimation and Risk Analysis 12 - 8 It is often difficult to quantify market risk.

In this case, the addi- tional income that would actually flow to the downtown office should be at- tributed to the branch. This is an opportunity cost and it should be charged to the project. What type of risk is being measured? This time value is the change in the purchasing power of the dollar over time. One position was that inter- est should be deducted, resulting in the net cash flow to stockholders, and then that cash flow should be discounted at the cost of common equity. The project is the application of a radically new technology to a new type of solar water heater, which will be manufactured under a 4-year license from a university.

Capital Budgeting: Estimating Cash Flow & Analyzing Risk

Will taking on the project increase the firms and stockholders risk? This is more or less the discount rate at which the present value of cash outflows equals the present value of cash inflows. This suggests that investors, even those who are well diversified, consider fac- tors other than market risk when they establish required returns. BQC generally adds 3 percentage points to the corporate WACC when it evaluates projects deemed to be risky, so it recalculated the NPV using a 15 percent cost of capital. The firm is involved with materials and caulking compound is a building material, so it is a similar product to the firm's other products. We then typed all the labels into a spreadsheet and used the spreadsheet to do the calculations.

A numerical analysis may not capture all of the risk factors inherent in the project. In a scenario analysis, we begin with the base-case scenario, which uses the most likely value for each input variable. We could have used a calculator and paper, but Excel is mucheasier when dealing with realistic capital budgeting problems. The ranges for each variable are then plotted, with the largest range on top and the smallest range on the bottom. Managers, not computers, make the final decision on whether to accept of reject projects. Requirement 2: Compute the Payback Period, Discounted Payback Period, NPV, IRR, and MIRR, if WACC is 10%. Sample Problem Replacement Project : Austen Inc.

If the project can be housed in an empty building that the firm owns and could sell if it were not used for the project, then this is an opportunity cost which should also be considered as a "cost" of this project. The difference between the required increase in operating current assets and the in- crease in operating current liabilities is the change in net operating working capital. Most decision makers do aquantitativeanalysis of stand-alone risk and then consider the other two types of risk in aqualitativemanner. However, for reasons that will become obvious as you go through the chapter, in practice spreadsheets are virtually always used. We then ask marketing, engineering, and other op- erating managers to specify a worst-case scenario low unit sales, low sales price, high variable costs, and so on and a best-case scenario. A time line with daily cash flows would in theory be most accu- rate, but daily cash flow estimates would be costly to construct, unwieldy to use, and probably no more accurate than annual cash flow estimates because we simply cannot forecast well enough to warrant this degree of detail. Uncertainty about a projects future profitability.

Cash Flow Estimation And Risk Analysis [wl1pk3m385lj]

Still, the water heater has the potential for being quite profitable, though it could also fail miserably. When a new project takes sales from an existing product, this is often called cannibalization. All this illustrates why government regulations are often necessary. Accept a capital investment when the PI is greater than 1, and reject it when the PI is less than 1. Costs of Fixed Assets Most projects require assets, and asset purchases represent negative cash flows. Should the cost be included in the analysis? Also, both suppliers and customers are reluctant to depend on weakfirms,andsuchfirmshavedifficultyborrowingmoneyatreasonable interest rates.

The graphs show the very wide range of pos- sibilities, indicating that this is indeed a very risky project. This feature of the tax code is set to expire before this book will be printed, but Congress has extended the bonus once and might extend it again. They are part of the costs of capital. Therefore, one could argue that daily cash flows would be better than annual flows. Why is it important to include inflation when estimating cash flows? Sales taxes, property taxes, and income taxes also fell, negatively affecting cities and states as well as the federal government. But for projects with highly predictable cash flows, such as constructing a building and then leasing it on a long-term basis with monthly payments to a finan- cially sound tenant, we would analyze the project using monthly periods. WACC Net investment in fixed assets depreciable basis Required new working capital Straight-line deprec.

Cash Flow Estimation and Risk blog.sigma-systems.com

Empirical studies of the determinants of required rates of return k gen- erally find that both market and corporate risk affect stock prices. A numerical analysis may not capture all of the risk factors inherent in the project. Sensitivity, scenario, and simulation analyses all ignore diversification. We see, then, that we need to extend sensitivity analysis to deal with the probability distributions of the inputs. Project remains acceptable after accounting for differential higher risk. Interest Charges Are Not Included in Project Cash Flows.

However, it is limited in that it considers only a few discrete outcomes NPVs , even though there are an infinite number of possibilities. Normally, additional inventories are required to support a new operation, and expanded sales tie up additional funds in accounts receivable. Cash Flow Projections: Base Case We usedExcelto do the analysis. We discuss them in the sections that follow. Finance, politics, and the environment are all interconnected. Additional Problem 7 Rachel Inc. It was demonstrated that equity flows discounted at the equity cost and operating flows discounted at the WACC led to the same conclusions.

It shows the ratio of the present value of cash inflows to the present value of cash outflows. The after-tax sales amount for this building will reduce the project's NPV. Many of these packages are included as add-ons to spreadsheet programs such as Microsoft Excel. Growth options permit a project to be expanded if demand turns out to be stronger than expected. Others are more speculative—units sold and the variable cost per- centage are in this category.

:max_bytes(150000):strip_icc()/DCF-f7593de5b9444e378b90a237a9bd83f6.png)