In economics, the long run equilibrium price is the price at which the supply and demand for a good or service are in balance, and there is no incentive for producers or consumers to change their behavior. In the long run, all factors of production are variable, meaning that firms can adjust their level of production by changing the amount of inputs they use, such as labor and capital.

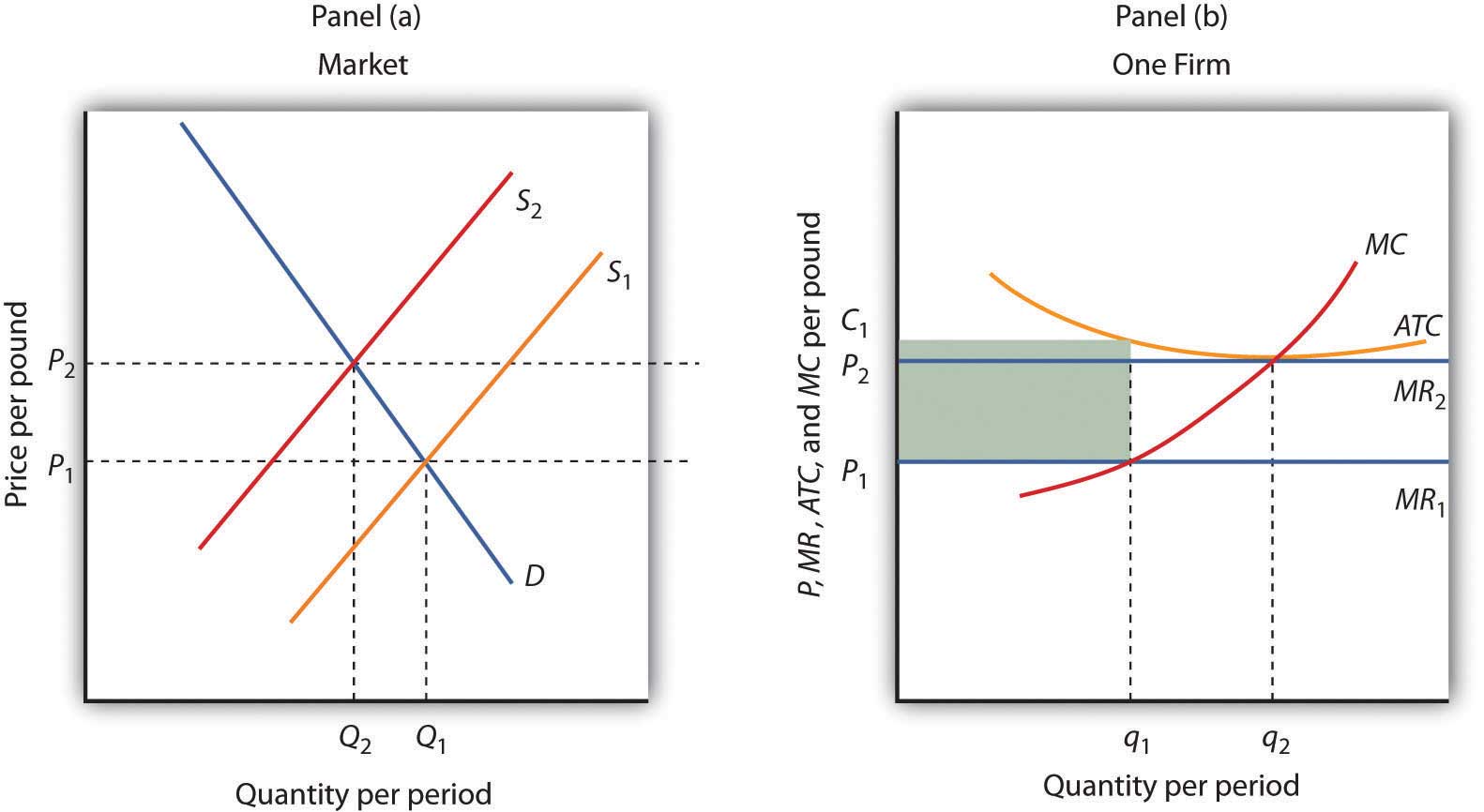

In the long run, firms will enter or exit a market based on their expectations of future profits. If the price of a good or service is above the long run equilibrium price, firms will enter the market to take advantage of the higher prices. This increase in the number of firms will lead to an increase in the supply of the good or service, which will ultimately drive down the price. On the other hand, if the price is below the long run equilibrium price, firms will exit the market because they are not able to earn sufficient profits. This reduction in the number of firms will lead to a decrease in the supply of the good or service, which will drive up the price.

In the long run, the forces of supply and demand will work to bring the price of a good or service to its equilibrium level. At this point, there is no incentive for producers to change the quantity of the good or service they produce, and there is no excess demand or supply. In other words, the market is in a state of equilibrium.

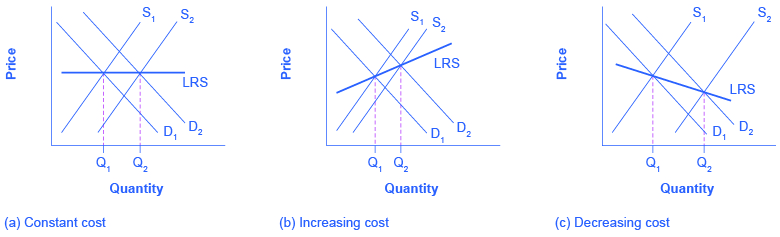

One of the key characteristics of the long run equilibrium price is that it is not fixed, but rather it is constantly changing as the underlying factors of production and consumer preferences evolve. For example, if there is a technological innovation that makes it easier and cheaper to produce a good or service, the supply curve will shift to the right, leading to a lower long run equilibrium price. On the other hand, if there is an increase in the cost of inputs, the supply curve will shift to the left, leading to a higher long run equilibrium price.

In summary, the long run equilibrium price is the price at which the supply and demand for a good or service are in balance in the long run. It is determined by the underlying factors of production and consumer preferences, and it is constantly changing as these factors evolve. Understanding the concept of long run equilibrium price is important for firms that want to make informed decisions about production and pricing, as well as for policymakers who want to understand the forces that drive the economy.